Operating a business without insurance is like driving a vehicle without a seatbelt; it’s okay until it’s not. By 2026, serious business owners will have no choice but to understand the 5 types of business insurance that protect companies from financial disasters. The right coverage from these 5 types of business insurance can mean the difference between recovery and permanent closure — whether you run a small retail store, a growing manufacturing unit, or a professional consulting firm.

In this guide, we break down the 5 types of business insurance in simple terms, explain who needs each policy, and share real-world examples so you can choose the right protection with confidence.

Table of Contents

What Is Business Insurance? (Meaning and Importance)

Business insurance meaning, in its simplest form, is a contractual arrangement between a business and an insurer where the business pays regular premiums in exchange for financial protection against unexpected losses. To fully understand how protection works, it’s important to look at the 5 types of business insurance, as each type covers different risks a company may face.

These losses could arise from lawsuits, property damage, employee accidents, natural disasters, or operational disruptions. The insurer steps in to cover eligible costs up to the policy limit, shielding the business from financial ruin — which is why knowing the right 5 types of business insurance for your operations is essential.

Why Businesses Need Insurance

- Legal liability: A single lawsuit can cost lakhs or even crores in legal fees and settlements.

- Asset protection: Fire, theft, and floods can destroy years of investment overnight.

- Employee obligations: Most countries and states require coverage for worker injuries.

- Client and contract requirements: Many contracts mandate professional indemnity or liability coverage before work begins.

- Business continuity: Interruption coverage keeps your income flowing even when your doors are closed.

| Quick Summary: Business Insurance Benefits – Protects personal and business assets from lawsuits – Ensures legal compliance with local labour and commercial laws – Builds trust with clients, investors, and partners – Reduces financial risk from unexpected events – Supports faster recovery after disasters or disruptions |

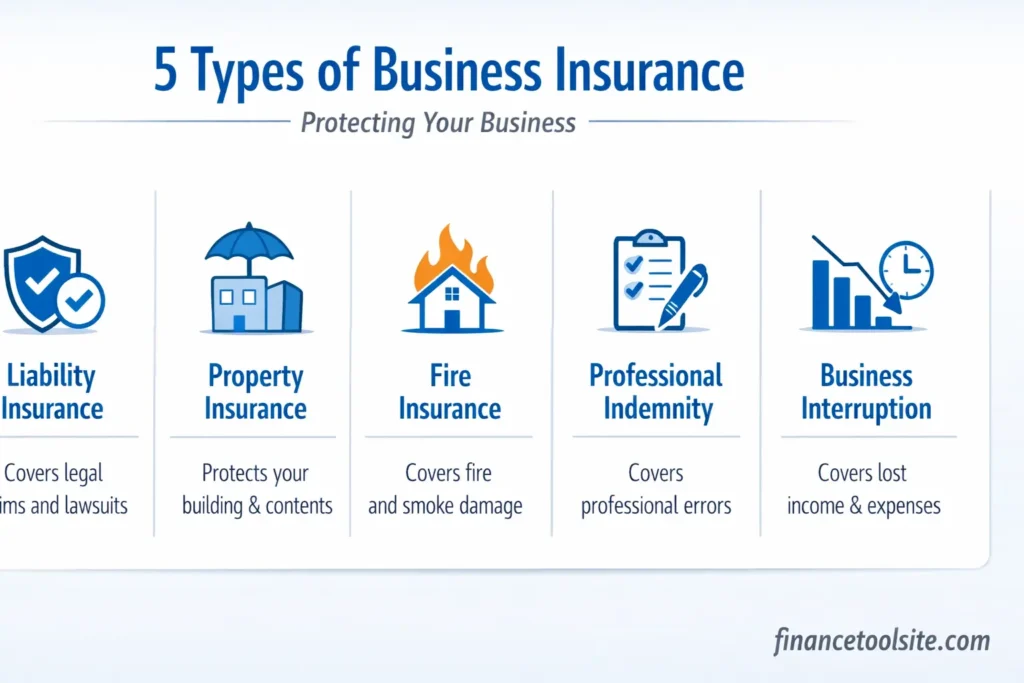

5 Types of Business Insurance: A Complete Breakdown

Below is a detailed explanation of the 5 types of business insurance that every small business owner should understand before purchasing a policy.

1. General Liability Insurance (Business Liability Insurance)

Business liability insurance is the most fundamental form of coverage and the starting point for any business. It protects your company against third-party claims of bodily injury, property damage, and advertising injury.

What it covers:

- A customer slipping and injuring themselves on your premises

- Damage your employee accidentally causes to a client’s property

- Claims of libel or slander in your advertising

- Legal defence costs, even for unfounded claims

Who needs it: Every business — from freelancers and home-based startups to large corporates.

Real-World Example: A café owner in Mumbai faces a lawsuit after a customer slips on a wet floor and breaks their wrist. General liability insurance covers the medical expenses and legal fees, which would otherwise run into several lakhs of rupees.

Key benefits: Low premium relative to coverage, broad applicability, and often required by landlords before signing a commercial lease.

2. Commercial Property Insurance

Commercial property insurance protects your physical business assets — the building, equipment, furniture, inventory, and electronics — from damage or loss due to fire, theft, vandalism, storms, and other covered perils.

What it covers:

- Office buildings or retail shop premises (owned or rented)

- Business equipment such as computers, machinery, and tools

- Stock and inventory damaged due to fire or flood

- Signage, furniture, and fixtures

Who needs it: Any business with a physical location or significant physical assets. This includes retailers, manufacturers, restaurants, and offices.

Real-World Example: A textile manufacturer in Surat loses machinery worth Rs. 40 lakh in a warehouse fire. Commercial property insurance covers the cost of repair and replacement, allowing the business to resume operations within weeks rather than closing permanently.

Key benefits: Covers fire insurance for business (a major peril in India), theft, and natural calamity damages. Can be tailored to include specific assets.

3. Professional Indemnity Insurance

Professional indemnity insurance, also called errors and omissions (E&O) insurance, protects professionals and service-based businesses against claims arising from mistakes, negligence, or failure to deliver services as promised.

What it covers:

- Errors or omissions in professional services or advice

- Breach of professional duty claims

- Copyright or intellectual property infringement in work delivered

- Legal costs and settlements in professional negligence cases

Who needs it: IT consultants, architects, lawyers, chartered accountants, financial advisors, doctors, and any business providing professional services.

Real-World Example: A software development firm in Bengaluru delivers a faulty module that causes a client’s e-commerce platform to go down for two days during a peak sale. The client sues for lost revenue. Professional indemnity insurance covers the legal costs and agreed settlement.

Key benefits: Covers costs that general liability does not, particularly those arising from intellectual or advisory work. Increasingly required in client contracts.

4. Workers’ Compensation Insurance

Workers’ compensation insurance covers employees who are injured or fall ill as a direct result of their work. It covers medical treatment, rehabilitation, and a portion of lost wages during recovery.

What it covers:

- Medical expenses for work-related injuries or illnesses

- Partial wage replacement during recovery

- Rehabilitation and physiotherapy costs

- Death benefits payable to the family of a deceased worker

Who needs it: Any business that employs staff, whether full-time, part-time, or contractual. In India, the Employees’ Compensation Act mandates this coverage for several categories of workers.

Real-World Example: A construction worker in Chennai fractures his arm on site. Workers’ compensation covers his hospitalisation, surgery, and two months of lost wages, protecting both the worker and the employer from financial and legal complications.

Key benefits: Legal compliance, employee trust, and protection from costly lawsuits arising from workplace injuries.

5. Business Interruption Insurance

Business interruption insurance — sometimes called business income insurance — compensates for lost revenue when your business is forced to halt operations due to a covered event such as fire, flooding, or storm damage.

What it covers:

- Lost net income during the period of interruption

- Fixed operating expenses like rent, salaries, and utility bills

- Temporary relocation costs if you need to operate from a different location

- Loan repayments that continue regardless of business closure

Who needs it: All businesses, but particularly those with high fixed costs or those that depend entirely on a single physical location, such as restaurants, retail outlets, and clinics.

Real-World Example: A restaurant in Kolkata suffers severe water damage from monsoon flooding. Business interruption insurance pays the owner’s monthly rent, staff salaries, and estimated revenue loss for the three months it takes to repair and reopen.

Key benefits: Keeps your business financially afloat during forced closure, reducing the risk of permanent shutdown.

5 Types of Business Insurance: Quick Comparison Table

| Insurance Type | What It Covers | Best For | Mandatory? |

| General Liability | Third-party injury, property damage, legal claims | All businesses | No (recommended) |

| Commercial Property | Office, equipment, inventory, fire, theft | Businesses with physical assets | No |

| Professional Indemnity | Errors, omissions, professional negligence | Consultants, IT, finance, legal | Yes, for some professions |

| Workers’ Compensation | Employee injuries, medical costs, lost wages | Businesses with employees | Yes, in many states/countries |

| Business Interruption | Lost income during forced closures | All businesses, esp. SMEs | No (strongly advised) |

Types of Business Insurance in India

The Indian insurance market is regulated by the Insurance Regulatory and Development Authority of India (IRDAI). Businesses in India can access a wide range of commercial insurance products, though penetration remains relatively low among micro and small enterprises.

Common types of business insurance in India include fire and special perils insurance, marine cargo insurance (for importers/exporters), product liability insurance, and public liability insurance. Under the Government of India’s MSME portal, small businesses can access information on credit guarantee and protection schemes that complement private insurance coverage.

Fire insurance for business is among the most widely purchased commercial policies in India, particularly in manufacturing and storage-heavy sectors. The IRDAI mandates that all insurers operate transparently and settle claims within defined timelines, ensuring policyholders are protected.

How to Choose the Right Business Insurance Coverage

There is no single policy that fits every business. The right combination depends on the nature of your operations, the assets you hold, the people you employ, and the clients you serve.

Consider these factors when assessing your coverage needs:

- Industry and risk profile: A construction firm faces very different risks than a digital marketing agency.

- Business size and revenue: Larger businesses often need higher coverage limits.

- Number of employees: More employees typically means greater workers’ compensation exposure.

- Client contracts: Many enterprise clients require specific liability or indemnity coverage before onboarding vendors.

- Location: Businesses in flood-prone or seismically active areas may need additional coverage extensions.

To get a precise estimate based on your specific profile, you can calculate your business insurance premium using an online tool that accounts for your industry, location, and coverage requirements.

Common Mistakes Business Owners Make with Insurance

- Underinsuring assets: Insuring equipment at purchase value rather than current replacement cost leaves significant gaps.

- Skipping business interruption coverage: Many owners assume property insurance is sufficient, not realising it does not cover lost income.

- Ignoring professional indemnity: Service businesses often overlook this until a client files a negligence claim.

- Not reviewing policies annually: Business growth, new locations, or new product lines can leave existing policies inadequate.

- Choosing solely on premium cost: The cheapest policy often has the most exclusions and lowest claim support.

Factors Affecting Your Business Insurance Premium

Insurance premiums are not arbitrary. Underwriters assess several risk factors before quoting a price:

- Industry sector and associated risk level

- Annual turnover and total insured value

- Number of employees and their roles

- Claims history over the past three to five years

- Location and exposure to natural disasters or crime

- Type and amount of coverage selected

- Security measures and safety protocols in place

| Key Takeaway: Business Insurance Benefits Business insurance is not an expense — it is an investment in operational resilience. The right mix of the 5 types of business insurance protects your assets, workforce, revenue, and professional reputation. A single uninsured incident can cost more than a decade of premiums combined. |

Frequently Asked Questions (FAQ)

What are the 4 types of business insurance?

While this article covers 5 types of business insurance, the four most commonly referenced are: general liability insurance, commercial property insurance, workers’ compensation insurance, and professional indemnity insurance. Business interruption insurance is increasingly considered a fifth essential category.

What is the meaning of business insurance?

Business insurance meaning refers to a set of policies that financially protect a company against losses arising from accidents, lawsuits, property damage, employee injuries, and operational disruptions. It allows businesses to manage risks without bearing the full financial burden themselves.

What are the types of business insurance in India?

Types of business insurance in India include fire and special perils insurance, public liability insurance, professional indemnity insurance, workers’ compensation (governed by the Employees’ Compensation Act), marine cargo insurance, and group health insurance for employees. IRDAI regulates all commercial insurers in India.

Can you give a business insurance example?

A business insurance example: A Delhi-based IT consultancy is sued by a client for delivering a software system with critical errors that caused financial loss. The firm’s professional indemnity insurance covers legal defence fees and the Rs. 15 lakh settlement, saving the business from severe cash flow disruption.

What is fire insurance for business?

Fire insurance for business is a specific policy or an add-on that covers damage to business property caused by fire, including building structures, machinery, inventory, and furniture. It is one of the most important coverages for manufacturers, warehouses, restaurants, and retailers in India.

What are the main benefits of business insurance?

Business insurance benefits include legal protection from third-party claims, asset recovery after disasters, employee welfare through compensation coverage, compliance with statutory requirements, and continuity of income during forced closures. It also strengthens credibility with clients and financial institutions.

Is business insurance mandatory in India?

Not all business insurance is mandatory in India. However, workers’ compensation (Employees’ Compensation Act), public liability (for certain industries), and fire insurance (for mortgaged properties) are required by law or lenders in specific circumstances. Other coverages, while not mandatory, are strongly advisable for all businesses.

| Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Insurance requirements vary by jurisdiction, industry, and business profile. Please consult a licensed insurance advisor or broker before making coverage decisions. |