You’ve heard about SIP a hundred times. You know it’s one of the easiest ways to build wealth. But the moment someone asks, “How much will ₹5,000 per month actually become in 10 years?” — most people have no clear answer. That’s exactly where the hdfc dream sip calculator comes in. It removes the guesswork and shows you real numbers in seconds.

Whether you’re just starting your SIP journey or trying to increase your monthly investment after a salary hike, this guide will show you everything step by step — from real examples to simple calculations you can actually understand.

And the best part? You don’t need Excel or complicated formulas anymore.

Table of Contents

What is the hdfc dream sip calculator?

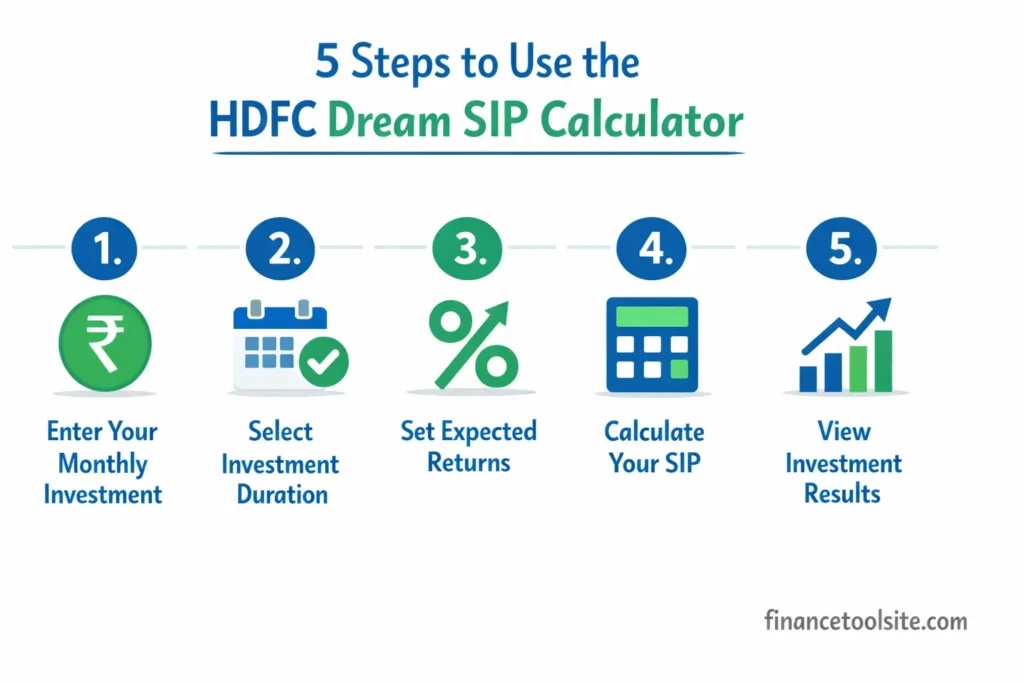

Here’s how to calculate your SIP returns in seconds:

- Open a SIP calculator (use the free tool above)

- Enter your monthly investment (e.g., ₹5,000)

- Select your investment duration (e.g., 10 years)

- Add expected return (usually 10–12% for long-term equity funds)

- Click calculate → instantly see total investment + returns

- Adjust for inflation if you want realistic future value

The hdfc dream sip calculator is a simple online tool that helps you estimate how much your monthly SIP can grow over time.

You enter three basic inputs:

- monthly investment amount

- investment duration

- expected rate of return

Based on these, the tool shows your total investment, estimated returns, and final maturity value.

What most people don’t realize is that this calculator is not limited to HDFC funds. It works on a standard SIP calculation method used across all mutual funds in India. As per guidelines from Securities and Exchange Board of India, SIP returns depend on market performance and compounding, not on any specific bank or platform.

This means the same calculation applies whether you invest in HDFC, SBI, ICICI, or any other fund.

So instead of focusing on the brand, the more important thing is getting an accurate estimate of your returns before you invest.

You can calculate it instantly here:

Calculate SIP Returns → financetoolsite.com/sip-calculator/

What Does It Actually Calculate?

A SIP calculator typically shows three key values:

- Total investment: the amount you put in over time

- Estimated returns: the gains based on expected growth rate

- Final value: total corpus at the end of the investment period

Some calculators also show inflation-adjusted value, which helps you understand the real future value of your money.

Simple Way to Understand It

Instead of guessing whether ₹3,000 or ₹5,000 per month will be enough for your goal, you can enter the numbers and get a clear answer within seconds.

That is the real purpose of the hdfc dream sip calculator — to give clarity before you start investing.

Use Our Free SIP Calculator — Faster Than the HDFC Tool

Before getting into formulas and detailed examples, it makes more sense to actually see the numbers in action.

If you’ve already opened the calculator above, you can test this while reading.

A good SIP calculator should not just give you a final number — it should help you understand how your money grows over time.

Here’s what a proper SIP calculator allows you to do:

- Calculate returns for any monthly investment, whether it’s ₹500 or ₹50,000

- Adjust the investment period from short-term (1–3 years) to long-term (20+ years)

- Try different return scenarios (for example, 8%, 12%, or 15%) to see realistic outcomes

- View how your investment grows year by year, not just the final amount

- Understand the difference between total investment and actual profit

Most bank calculators, including those from large financial institutions, are quite basic. They usually give you a single output number without much context.

A better approach is to use a calculator that shows a clear breakdown, so you can make decisions based on actual numbers instead of assumptions.

How to Calculate SIP Returns — The Simple Formula

If you’ve ever searched for the SIP return formula and felt confused, you’re not alone. The formula looks complex at first, but once you break it down, it’s actually straightforward.

The SIP Formula

M=P×(r(1+r)n−1)×(1+r)

What Each Variable Means

- M = Final maturity value (total amount you receive)

- P = Monthly SIP amount

- r = Monthly interest rate (annual return ÷ 12 ÷ 100)

- n = Total number of months

Step-by-Step Example

Let’s calculate returns for a ₹5,000 monthly SIP at 12% annual return for 10 years.

- Monthly rate (r) = 12 ÷ 12 ÷ 100 = 0.01

- Total months (n) = 10 × 12 = 120

Now applying the formula:

- (1.01)^120 ≈ 3.3004

- [(3.3004 – 1) ÷ 0.01] = 230.04

- Final value (M) = 5000 × 230.04 × 1.01 ≈ ₹11,61,695

Final Breakdown

- Total invested = ₹5,000 × 120 = ₹6,00,000

- Estimated returns = ₹5,61,695

- Final value = ₹11,61,695

That’s almost double your investment — purely through disciplined monthly investing and compounding.

What Most People Get Wrong

The formula is useful for understanding how SIP works, but in real life, very few people calculate this manually every time.

Even a small change in return rate or duration can completely change the final number. That’s why most investors prefer using a calculator instead of doing repeated manual calculations.

Practical Takeaway

You don’t need to memorize this formula.

What matters is understanding:

- how returns are calculated

- how time impacts growth

- and how small monthly investments can scale over years

Once you understand this, using a calculator becomes much more meaningful — because you know what the numbers actually represent.

HDFC Dream SIP Calculator Example — ₹5,000 Monthly Investment

Let’s look at a simple, real-world example so you can clearly understand how the hdfc dream sip calculator works in practice.

Scenario

Rahul, 28, earns ₹45,000 per month. He decides to invest ₹5,000 monthly through SIP for his child’s education goal, which is 10 years away. He assumes an average annual return of 12%, which is considered reasonable for long-term equity mutual funds.

Investment Details

- Monthly SIP: ₹5,000

- Investment duration: 10 years

- Expected annual return: 12%

Estimated Results

- Total invested: ₹6,00,000

- Estimated maturity value: ₹11,61,695

- Wealth gained: ₹5,61,695

- Return on investment: ~93.6%

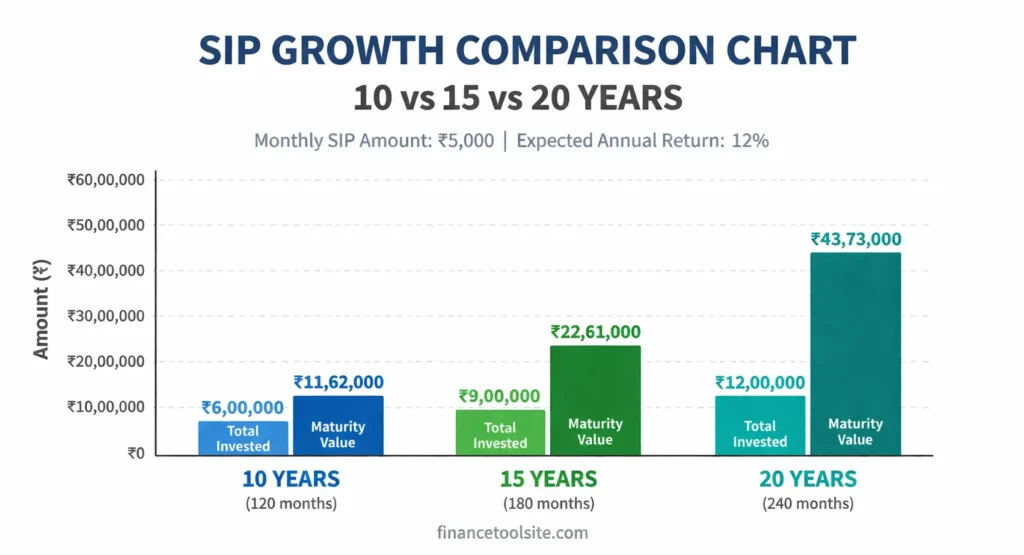

What Happens If He Stays Invested Longer?

| Tenure | Total Invested | Estimated Value | Profit |

|---|---|---|---|

| 10 Years | ₹6,00,000 | ₹11,61,695 | ₹5,61,695 |

| 15 Years | ₹9,00,000 | ₹25,22,880 | ₹16,22,880 |

| 20 Years | ₹12,00,000 | ₹49,95,740 | ₹37,95,740 |

What This Example Shows

The biggest takeaway here is not just the return — it’s the impact of time.

Rahul’s investment grows steadily in the first 10 years, but the real acceleration happens when he stays invested longer. This is the effect of compounding, where returns start generating their own returns.

Long-term investing through SIPs is widely encouraged in India for goals like education and retirement, as highlighted by Reserve Bank of India in its financial awareness initiatives focusing on disciplined investing and long-term wealth building.

Practical Insight

Most people focus only on “how much to invest.”

But in reality, two things matter more:

- how long you stay invested

- how consistently you invest

That’s exactly what the hdfc dream sip calculator helps you understand — the long-term impact of your decisions before you actually commit your money.

SIP Calculator India vs HDFC vs Groww vs Bajaj — Which is Best?

If you’ve searched for a SIP calculator before, you’ve probably come across platforms like HDFC Bank, Groww, or Bajaj Finserv.

All of them offer SIP calculators, but the experience and features can be quite different.

Here’s a simple comparison:

| Feature | HDFC Dream SIP | Groww SIP Calculator | Bajaj Finance Calculator | Typical Advanced Calculator |

|---|---|---|---|---|

| Monthly SIP Input | Yes | Yes | Yes | Yes |

| Inflation Adjustment | No | No | Partial | Yes |

| Year-by-year Breakdown | No | Yes | No | Yes |

| Download/Share Results | No | Yes | No | Yes |

| Comparison Mode | No | No | No | Yes |

| No Signup Required | Yes | Yes | Yes | Yes |

| Ad-free Interface | No | No | No | Yes |

What Actually Matters in a SIP Calculator

The important thing to understand is this:

All calculators — whether from banks or fintech platforms — use the same underlying SIP formula. The final result will be similar if the inputs are the same.

The real difference comes down to:

- how clearly the results are presented

- whether you can see a full breakdown

- how easy it is to test different scenarios

Some calculators are designed mainly to promote specific products, while others focus more on helping users understand their numbers better.

Practical Takeaway

Instead of focusing on which brand’s calculator you’re using, focus on whether it actually helps you:

- understand your returns clearly

- compare different investment durations

- make better financial decisions

A good SIP calculator should simplify your decision-making — not just give you a final number.

Benefits of SIP Investment (Why Every Indian Should StarBenefits of SIP Investment (Why Every Indian Should Start Today)

You already know what SIP is. But here’s why it actually works for regular Indians — not just high-income earners:

- Rupee Cost Averaging: When markets fall, you automatically buy more units. When they rise, your existing units grow in value. This helps balance your average cost over time.

- Power of Compounding: The longer you stay invested, the higher your returns. Even ₹1,000/month started early can outperform ₹5,000/month started late.

- Disciplined Investing: SIP turns investing into a habit. Your money gets invested automatically before you spend it.

- Low Entry Barrier: Many funds allow SIPs from ₹100–₹500. You don’t need a large amount to start.

- Flexibility: You can increase, pause, or stop your SIP anytime based on your situation.

- Better Long-Term Potential Than FD: Over long periods, equity mutual funds have generally delivered higher returns than fixed deposits, as also highlighted by Association of Mutual Funds in India.

SIP Calculator with Inflation — Don’t Ignore This

Here’s a mistake most first-time investors make: they calculate SIP returns but ignore inflation.

If inflation is around 6% per year, ₹50 lakhs in the future won’t have the same value as ₹50 lakhs today. Your actual purchasing power will be lower.

How to Calculate SIP Returns Adjusted for Inflation

| Without Inflation Adjustment | With Inflation (6%) |

|---|---|

| Expected return: 12% | Real return ≈ 6% |

| ₹5,000/month × 10 years | ₹5,000/month × 10 years |

| Maturity value: ₹11,61,695 | Inflation-adjusted value: ~₹8,20,000 |

The difference is significant.

This is why the hdfc dream sip calculator becomes more useful when you factor in inflation along with expected returns. It gives you a more realistic idea of what your investment will actually be worth in the future.

Common Mistakes While Calculating SIP Returns

Even if you’re using the best hdfc dream sip calculator, these common mistakes can lead to unrealistic projections:

- Using too optimistic a return rate: Assuming 18–20% returns is unrealistic. Historically, equity mutual funds have delivered around 12–14% over long periods. For safer planning, use 10–12%.

- Ignoring exit load and expense ratio: Mutual funds charge annual fees (usually 0.5%–1.5%). This slightly reduces your actual returns, so it should be considered.

- Not accounting for tax: Long-term capital gains (LTCG) above ₹1 lakh are taxed at 10%. Your final amount will be slightly lower than what the calculator shows.

- Stopping SIP during market crashes: This is one of the biggest mistakes. Market declines allow you to buy more units at lower prices. Stopping your SIP breaks the compounding process.

- Not reviewing your SIP regularly: If your income has increased over time, your SIP amount should also increase. Reviewing your plan annually helps you stay aligned with your goals.

FAQs — HDFC Dream SIP Calculator

What is the HDFC Dream SIP Calculator?

The hdfc dream sip calculator is an online tool that estimates how much your monthly SIP can grow over time based on your investment amount, duration, and expected returns. It helps you get a clear idea of your future corpus before you start investing.

How to calculate SIP returns manually?

SIP returns are calculated using the formula:

M = P × {[(1 + r)^n – 1] / r} × (1 + r)

where P is the monthly investment, r is the monthly interest rate, and n is the total number of months. For example, ₹5,000 per month at 12% for 10 years gives approximately ₹11,61,695.

Is SIP better than FD in India?

For long-term goals (5+ years), SIPs in equity mutual funds have historically delivered higher returns than fixed deposits. FDs typically offer around 6–7%, while equity funds have delivered around 12–15% over long periods. However, SIPs involve market risk, while FDs are more stable and predictable.

How much will ₹5,000 SIP grow in 10 years?

At an expected return of 12%, ₹5,000 per month for 10 years grows to approximately ₹11,61,695. The total investment is ₹6,00,000, and the returns are about ₹5,61,695.

Is the SIP calculator with inflation feature important?

Yes. Without adjusting for inflation, you may overestimate the real value of your future corpus. If inflation is 6% and your return is 12%, your effective return is closer to 6%. This gives a more realistic view of your purchasing power.

Final Word — Start Calculating, Start Investing

The biggest reason people delay investing isn’t lack of money — it’s lack of clarity.

Once you understand how small monthly investments grow over time, the decision becomes much easier. SIP is not about timing the market or investing large amounts. It’s about consistency, patience, and giving your money enough time to compound.

Even a simple ₹2,000–₹5,000 monthly investment, if continued for years, can build a meaningful corpus. The key is to start early, stay consistent, and increase your investment gradually as your income grows.

You don’t need perfect conditions to begin. You just need a clear plan and the discipline to stick with it.

Disclaimer: This content is for educational purposes only and does not constitute financial advice. Mutual fund investments are subject to market risks. Always do your own research or consult a financial advisor before making investment decisions.