Many accounting students and even working accountants often get confused about insurance under which head in Tally when they try to create an insurance ledger in Tally Prime. The confusion usually happens in the “Under” field, where you must select the correct ledger group. Choosing the wrong group can affect your Profit & Loss statement and make financial reports inaccurate.

Table of Contents

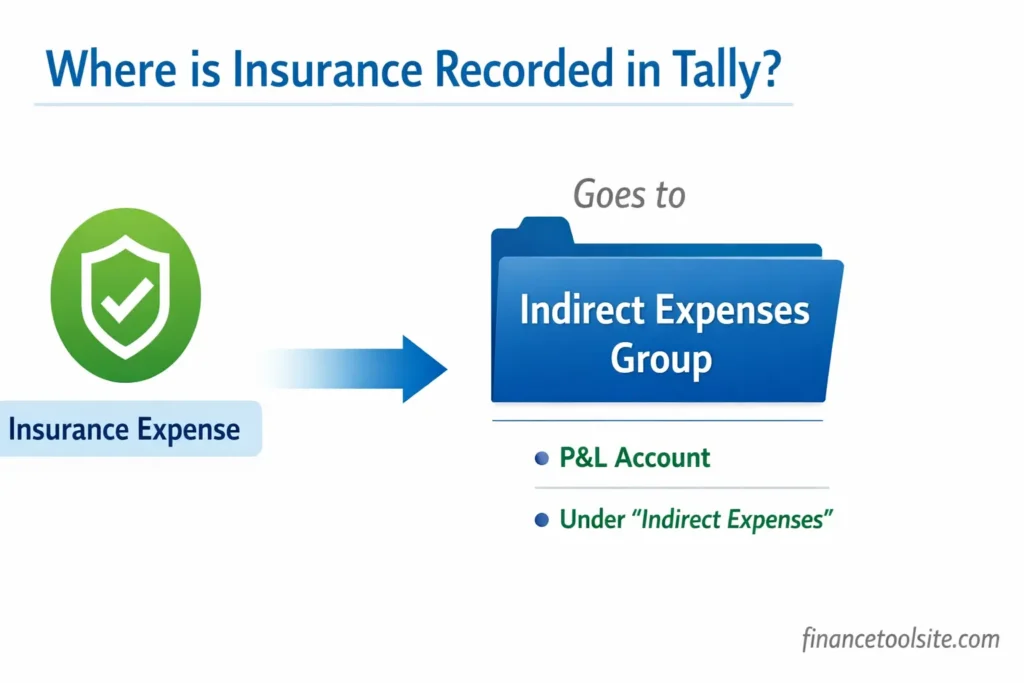

In most cases, insurance expenses in Tally are recorded under the Indirect Expenses group. This is the standard accounting treatment because insurance is considered a business overhead rather than a production cost. However, simply memorizing the ledger group is not enough — understanding why insurance is placed under this head helps accountants maintain accurate records and apply the same logic to other expenses in Tally.

If you are wondering insurance under which head in Tally, the short answer is:

Insurance → Indirect Expenses

Most businesses record insurance premiums under Indirect Expenses in Tally Prime because they are regular operating costs used to protect business assets such as buildings, vehicles, machinery, or stock.

However, there are some exceptions depending on the business type.

When discussing insurance under which head in Tally, the expense is generally classified under Indirect Expenses because insurance is treated as a revenue expenditure. This means the benefit of the expense is limited to the current accounting period and it does not create a long-term asset for the business.

For example, if a company pays insurance for its office building, vehicles, or inventory, the premium is considered an operational cost required to run the business safely.

In some manufacturing businesses, insurance related to factory machinery or production assets may sometimes be treated as a Direct Expense. This is because such insurance can be considered part of the production overhead and included in the cost of goods manufactured.

However, for most trading businesses, service companies, and small enterprises, the correct and widely accepted accounting treatment is to record insurance under Indirect Expenses in Tally Prime.

Why Insurance Goes Under Indirect Expenses — The Accounting Logic

Before working in Tally Prime, it is important to understand the accounting logic behind insurance under which head in Tally. Many beginners try to memorize the ledger group without understanding the concept, which later creates confusion when they have to classify other expenses.

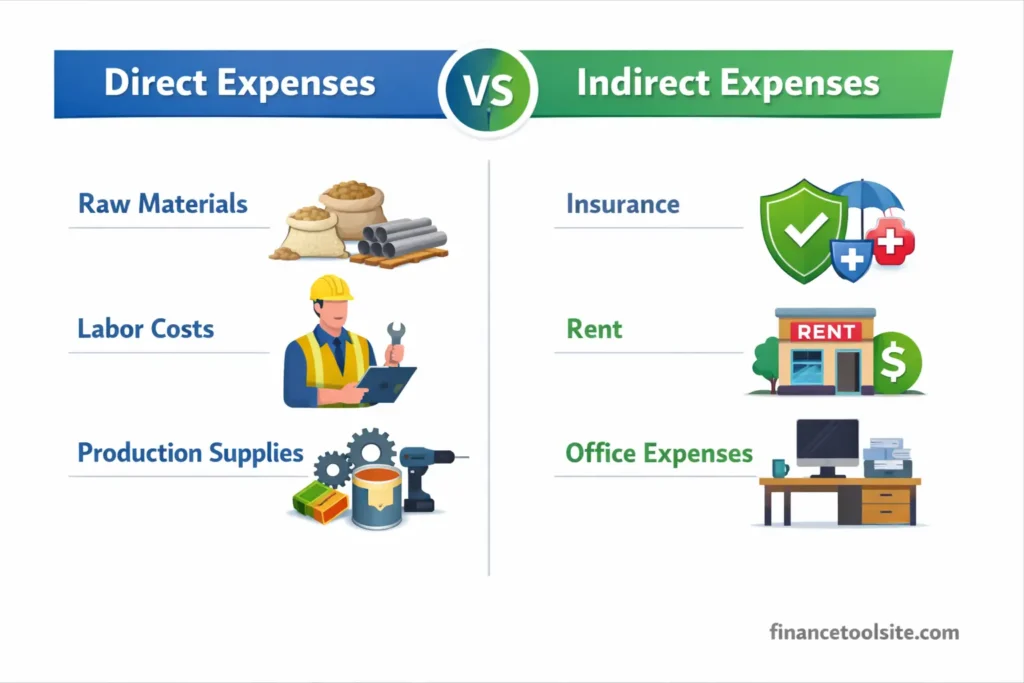

In accounting, business expenses are broadly divided into two main categories: Direct Expenses and Indirect Expenses.

- Direct Expenses are costs directly related to production or the core service of the business. Examples include raw materials, factory wages, freight inward, Production Supplies, and Labor Costs.

- Indirect Expenses are costs required to run the business operations but are not directly connected to manufacturing or service delivery. Examples include Insurance, Rent, and Office Expenses.

Understanding this difference makes it easier to decide insurance under which head in Tally Prime should be recorded.

Insurance premiums — whether they cover your office building, business equipment, vehicles, or stock — are usually treated as period costs in accounting. These policies protect business assets but do not directly contribute to producing goods or services. Because of this, insurance expenses are generally recorded under the Indirect Expenses group in Tally Prime.

In India, insurance companies and policies are regulated by the Insurance Regulatory and Development Authority of India (IRDAI), which oversees the insurance sector and ensures that policies follow regulatory standards. Businesses pay insurance premiums regularly to safeguard their operations against unexpected risks.

Think of it this way: even if your business stopped production for a few months, you would still need to pay the insurance premium to keep your coverage active. This clearly shows why insurance is considered an indirect operating cost rather than a production expense.

This is exactly why the question insurance under which head in Tally is commonly asked by accounting students and beginners.

However, there are a few exceptions. In manufacturing companies, insurance related to factory buildings, machinery, or production equipment may sometimes be treated as a Direct Expense because it forms part of the production overhead and can affect the cost of goods manufactured.

Despite this exception, for most trading businesses, service companies, and small enterprises, the correct and widely accepted accounting treatment is to record insurance under Indirect Expenses in Tally Prime.

Another situation arises when businesses pay insurance for employees as a staff benefit, such as employee health insurance or group life insurance. In such cases, the expense can still be recorded under Indirect Expenses, either within Staff Welfare Expenses or a separate ledger like Employee Insurance.

Before purchasing an insurance policy for employees or family members, many businesses compare policy costs to estimate the expected premium. You can use tools like the SBI Health Insurance Plans for Family Premium Calculator to estimate the premium amount.

If you want to understand all ledger groups used in Tally, you can also read our detailed guide on Tally Ledger Group List, which explains how different expenses and incomes are classified in Tally.

Step-by-Step: Creating an Insurance Ledger in Tally Prime

Once you understand insurance under which head in Tally, the next step is to create the correct ledger in Tally Prime. Setting up the ledger properly ensures that insurance expenses appear correctly in your Profit & Loss statement.

Follow the step-by-step process below to create an Insurance ledger in Tally Prime.

Steps to Create Insurance Ledger in Tally Prime

Step 1 – Open Tally Prime

Open Tally Prime and go to the Gateway of Tally for your company.

Step 2 – Open the Ledger Creation Screen

From the Gateway of Tally:

- Press Alt + G

- Select Create Master

- Click on Ledger

You can also access it through:

Gateway of Tally → Masters → Ledgers → Create

Step 3 – Enter the Ledger Name

In the Name field, enter a clear ledger name such as:

- Insurance Premium

- Insurance Expense

- Vehicle Insurance

Using clear names helps you easily identify the expense in financial reports.

Step 4 – Select the Correct Ledger Group

In the Under field, select:

Indirect Expenses

This is the most common ledger group used when recording insurance under which head in Tally Prime, because insurance is treated as a business operating expense.

You can simply start typing “Ind” and Tally will automatically filter and display Indirect Expenses in the list.

Step 5 – Inventory Option

Keep the Inventory Values Affected option set to No, because insurance is an expense and not related to inventory items.

Step 6 – Save the Ledger

Press Ctrl + A or click Accept to save the ledger.

Your Insurance Expense ledger is now ready to be used when recording insurance payments in Tally.

Quick Tip

Many businesses create separate ledgers for different types of insurance, such as:

{kind=link}

- Vehicle Insurance

- Building Insurance

- Stock Insurance

This helps track insurance expenses more accurately in financial reports.

Journal Entry for Insurance in Tally

After creating the ledger, the next step is recording the insurance payment entry in Tally Prime. Understanding the correct entry helps avoid mistakes in financial statements and ensures that the expense appears properly in the Profit & Loss account.

Let’s assume your business pays ₹15,000 as an annual insurance premium for the office building.

Insurance Journal Entry

| Particulars | Ledger Head | Debit (₹) | Credit (₹) |

|---|---|---|---|

| Insurance Premium A/c | Indirect Expenses | 15,000 | |

| To Bank / Cash A/c | Bank Accounts / Cash-in-Hand | 15,000 | |

| (Being annual insurance premium paid) |

This entry records the insurance premium as a business expense while reducing the balance of your bank or cash account.

How to Record Insurance Entry in Tally Prime

Follow these steps to record the transaction in Tally Prime:

- Go to Gateway of Tally.

- Open Accounting Vouchers.

- Select Payment Voucher (F5).

- In the Account field, choose your Bank Account or Cash Account.

- In the Particulars section, select the Insurance Premium ledger.

- Enter the amount and save the voucher.

This process records the insurance payment under Indirect Expenses, which is the correct classification for most businesses when determining insurance under which head in Tally.

Important Tip

If the payment is made through bank transfer, online banking, or UPI, the correct voucher type is Payment Voucher in Tally Prime.

Many businesses today also pay their premiums directly through the insurer’s online portal. For example, if your policy belongs to Tata AIA, you can complete the payment using Tata AIA Life Insurance Premium Payment Online and then record the transaction in Tally using the same payment entry method.

Insurance Claim or Refund Entry

If your company later receives an insurance claim or refund, the accounting treatment changes slightly.

In that case:

- Debit: Bank Account

- Credit: Insurance Claim Received (Indirect Income)

You would record this using a Receipt Voucher (F6) in Tally Prime.

Creating a separate ledger called Insurance Claim Received under Indirect Income helps keep insurance expenses and claim recoveries clearly separated in financial reports.

Real-World Example: How a Small Business Handles Insurance in Tally

To understand insurance under which head in Tally more clearly, let’s look at a practical example from a small business.

Suppose Mehta Electronics, a mid-sized trading business in Pune, purchases different insurance policies to protect its operations. The company has insurance coverage for its showroom premises, delivery vehicle, and stock-in-trade. Each policy has a different premium amount and renewal date.

Instead of recording everything under a single ledger, Mehta Electronics creates separate insurance ledgers in Tally Prime for better tracking and reporting.

Example Insurance Ledgers in Tally

- Showroom Insurance Premium — Under Indirect Expenses

- Vehicle Insurance Premium — Under Indirect Expenses

- Stock Insurance Premium — Under Indirect Expenses

Creating separate ledgers helps the business clearly understand how much it spends on each type of insurance during the financial year.

For example, before recording the vehicle insurance expense in accounts, businesses often estimate the expected premium amount. You can do this using tools like the Car Insurance Premium Calculator in Excel, which helps calculate an approximate policy cost before making the actual payment.

At the end of the year, this structure produces a clean and easy-to-read Profit & Loss statement, where each insurance cost is visible separately. While it is possible to maintain a single ledger called Insurance Expense, creating separate ledgers provides better clarity for budgeting, audits, and financial analysis.

Why Separate Insurance Ledgers Are Useful

Maintaining separate insurance ledgers in Tally Prime helps businesses:

- Track insurance costs for different assets

- Compare yearly insurance expenses

- Identify cost increases during policy renewal

- Prepare clearer financial reports for auditors

Because of these benefits, most professional accountants prefer separate insurance ledgers instead of one combined ledger.

Related Expense Tracking in Tally

Many small businesses also track banking charges and financial service fees separately to understand their total operational costs.

If you are unsure how these charges should be classified, you can read our detailed guide on Bank Charges Under Which Head in Tally, which explains the correct ledger group used in Tally.

To estimate your monthly banking costs, you can also use this simple tool: Bank Charges Calculator.

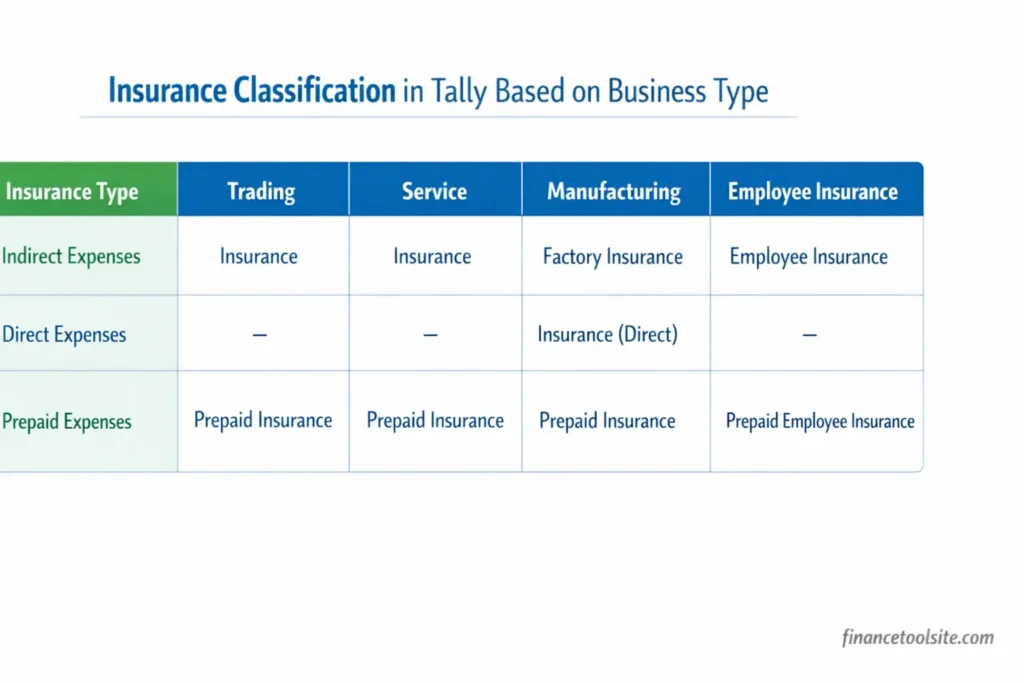

Insurance in Tally — Which Group Based on Business Type

When deciding insurance under which head in Tally, the correct ledger group can sometimes depend on the type of business and the purpose of the insurance policy. In most situations, insurance is recorded under Indirect Expenses, but certain cases may require a different classification.

The table below explains how insurance is generally classified in Tally Prime based on different business scenarios.

Insurance Ledger Group in Tally

| Business Type | Type of Insurance | Tally Group |

|---|---|---|

| Trading / Retail | Shop, stock, vehicle insurance | Indirect Expenses |

| Service / Consulting | Office insurance, professional indemnity | Indirect Expenses |

| Manufacturing | Factory machinery or plant insurance | Direct Expenses (Production Overheads) |

| Any Business | Employee health or life insurance | Indirect Expenses |

| Any Business | Prepaid insurance (future period) | Current Assets → Prepaid Expenses |

As you can see, Indirect Expenses remains the most commonly used group when recording insurance expenses in Tally.

Understanding Prepaid Insurance in Tally

The last row in the table often confuses many accountants.

For example, suppose your business pays a one-year insurance premium in March, but the policy period runs from April to March of the next financial year. In that case, the portion of the premium that belongs to the next accounting period should not be treated as an expense for the current year.

Instead:

- The current year portion is recorded under Indirect Expenses.

- The future period portion is recorded under Prepaid Expenses, which falls under Current Assets in Tally.

This accounting treatment ensures that expenses are recorded in the correct financial period.

The concept behind this is known as the Matching Principle in Accounting, which states that expenses should be recorded in the same accounting period as the revenue they help generate.

Understanding this principle also makes it easier to answer the common question insurance under which head in Tally, because the correct classification depends on both the nature of the expense and the accounting period to which it belongs.

Common Mistakes Accountants Make with Insurance in Tally

Even after understanding insurance under which head in Tally, many beginners and small business accountants still make mistakes while recording insurance transactions. These errors can affect financial statements and sometimes create confusion during audits.

Below are some of the most common mistakes accountants make when recording insurance in Tally Prime.

1. Recording Insurance Under Direct Expenses Unnecessarily

For most trading and service businesses, insurance has no direct connection with the production or purchase of goods.

If you record insurance under Direct Expenses, it can distort the Gross Profit (GP) ratio of the business. This ratio is closely examined by banks, auditors, and tax authorities, so incorrect classification may lead to misleading financial reports.

In most cases, the correct classification remains:

Insurance → Indirect Expenses

2. Creating the Ledger Under Sundry Creditors or Duties & Taxes

Another common mistake occurs when accountants confuse the insurance expense with the payment entry.

If the insurance premium is paid immediately, the correct entry is:

Debit: Insurance Premium (Indirect Expenses)

Credit: Bank or Cash Account

The Sundry Creditors group should only be used if the insurance company has issued an invoice but the payment has not yet been made. Even in that situation, the insurance expense ledger should still remain under Indirect Expenses.

3. Ignoring Prepaid Insurance Adjustment

When an insurance premium covers two financial years, some accountants record the entire amount as an expense in the year of payment.

However, under mercantile accounting, this is technically incorrect.

The correct treatment is:

- Current year portion → Indirect Expenses

- Future period portion → Prepaid Expenses (Current Assets)

Failing to adjust prepaid insurance can cause overstatement of expenses in one financial year and understatement in another.

4. Using One Generic “Insurance” Ledger for All Policies

Some businesses maintain a single ledger called Insurance Expense for every policy.

While this works technically, it makes financial analysis difficult.

A better practice is to create separate ledgers, such as:

- Vehicle Insurance

- Building Insurance

- Stock Insurance

This approach makes the Profit & Loss statement clearer and helps businesses track rising insurance costs more easily.

5. Forgetting TDS on Insurance Commission (When Applicable)

This mistake usually occurs in businesses related to insurance agency or brokerage services.

If a person earns insurance commission income, TDS under Section 194D of the Income Tax Act may apply. In such cases, the accounting treatment is different from regular insurance expense entries.

Therefore, accountants should ensure they do not mix insurance commission accounting with insurance premium expense entries in Tally.

Frequently Asked Questions

1. Insurance comes under which group in Tally?

Insurance comes under the Indirect Expenses group in Tally Prime and Tally ERP 9. It is a revenue expenditure that is matched to the accounting period in which it is incurred.

2. Can insurance be put under Direct Expenses in Tally?

Yes, but only in specific situations — typically in manufacturing businesses where insurance on factory plant or machinery is considered part of production overhead. For most businesses, Indirect Expenses is the correct group.

3. What is the journal entry for insurance paid in Tally?

Debit Insurance Premium A/c (Indirect Expenses) and Credit Bank/Cash A/c. If using a Payment voucher in Tally, the bank account is selected in the Account field, and the insurance ledger is added in the Particulars section.

4. How do I create an insurance ledger in Tally Prime?

Go to Gateway of Tally > Accounts Info > Ledgers > Create. Name it “Insurance Premium”, set the Under field to “Indirect Expenses”, and save. That’s it.

5. Is prepaid insurance an asset in Tally?

Yes. If a premium payment covers a future period beyond the current financial year, the unexpired portion is a Prepaid Expense — which is a Current Asset in Tally. Create a separate ledger under Current Assets > Prepaid Expenses for this.

6. What about GST on insurance premium? How does that work in Tally?

Insurance services attract GST (typically 18% for general insurance). When you record the payment, you’d need to split the entry into the base insurance premium and the GST input tax credit — only if your business is GST-registered and the insurance qualifies for ITC (which has restrictions for certain types like motor vehicles).

7. What if my company receives an insurance claim? Where does that go in Tally?

An insurance claim received is income. Create a ledger called “Insurance Claim Received” under Indirect Income (also called Other Income) in Tally. Debit your Bank account and credit this ledger using a Receipt voucher.

8. Is life insurance paid for a director or partner recorded under Indirect Expenses?

It depends on the business structure. Life insurance on a partner’s life taken by a partnership firm may not be allowed as a business expense under the Income Tax Act. In Tally, you can still record it under Indirect Expenses for accounting purposes, but your CA should advise on the tax treatment separately.

Wrapping Up

Recording insurance correctly in Tally isn’t complicated once you understand the underlying logic. It’s an Indirect Expense for most businesses — not a direct production cost, not a liability, and definitely not an asset (unless it’s prepaid). Create clean, purpose-specific ledgers, record each entry on time, and handle prepaid portions properly at year-end. Your P&L will thank you for it, and so will your auditor. If you’re trying to improve your overall financial knowledge as a business owner or accounting student, reading a good Money Management Book in Hindi can also help you understand how expenses, budgeting, and financial planning work together.

Disclaimer: This article is for educational purposes only and does not constitute professional accounting advice. Please consult a qualified Chartered Accountant for advice specific to your business situation.

3 thoughts on “Insurance Under Which Head in Tally? Ledger Group, Entry & Example (Tally Prime 2026)”