Your salary just got credited, and within a few days, most of it is already gone. No big shopping, no luxury spending—just regular expenses, and somehow your balance still drops faster than expected. If this feels familiar, you’re not alone. I’ve seen this pattern again and again, especially with people earning between ₹10,000 to ₹30,000 who genuinely want to save but can’t figure out how. That’s exactly why so many people search for how to save money fast on a low income—because the real problem isn’t just low income, it’s what happens after you receive it. In this article, I’ll show you a simple, practical system you can start using from your very next salary.

No fluff. No investment lectures. Just a direct, working system.

Table of Contents

How to Save Money Fast on a Low Income

Here’s the short version for those who need it right now:

- Transfer ₹500–₹1,000 to a separate savings account the moment your salary arrives

- List every fixed expense (rent, EMI, recharge, utility) and pay them first

- Set a strict daily cash limit for variable spending (food, travel, small purchases)

- Delete or log out of Swiggy, Zomato, and Amazon for at least 15 days a month

- Track every rupee using a notebook or free app like Walnut or Money Manager

- Cook at home even 3 extra days a week — saves ₹1,500 to ₹2,000 easily

- Never touch your savings account for impulse purchases

How to Save Money Fast on a Low Income in India

India has a unique money problem. UPI has made spending almost frictionless — and that’s dangerous when you’re trying to figure out how to save money fast on a low income. One tap and ₹500 disappears on food delivery. Another tap and ₹300 is gone on a mobile game or an OTT subscription you didn’t even realize was active.

I’ve worked with hundreds of people earning between ₹10,000 and ₹25,000 a month, and the pattern is almost always the same. It’s not just about income — it’s about what happens on day one. Most people don’t have an earning problem; they have a spending system problem, which is exactly why they struggle with how to save money fast on a low income in India.

In fact, studies on digital payment behavior — like insights shared by the National Payments Corporation of India — show how UPI has made everyday transactions faster and easier, but also more frequent, which increases the chances of small, unnoticed expenses adding up quickly.

Here are the biggest money leaks in low-income households:

- Food delivery (₹800–₹2,000/month for even one person)

- Unnecessary mobile data packs and OTT subscriptions

- Impulse shopping on Amazon and Meesho

- Tobacco, gutka, alcohol — often ₹1,500–₹3,000 monthly leaks that go unnoticed

- Social pressure — birthdays, weddings, and “going Dutch” lunches with colleagues

Fix just these five areas, and most people earning ₹15,000 can realistically save ₹2,000–₹3,500 per month. That’s ₹24,000–₹42,000 a year — which is exactly how people start building an emergency fund while learning how to save money fast on a low income.

How to Save Money Fast on a Low Income from Salary

Most people save what’s left after spending. That’s why most people save nothing.

The moment you flip this habit — save first, spend what remains — everything changes. This is the single most powerful concept in personal finance and it costs you nothing to apply.

Here’s a real salary-day action plan:

Within 30 minutes of salary credit:

- Transfer your fixed saving amount immediately (even ₹500 is fine to start)

- Pay rent or EMI if due within 3 days

- Recharge mobile, pay electricity — clear all fixed bills

- Set a weekly spending allowance for groceries and daily needs

- Whatever remains is your ‘live on this’ money for the rest of the month

Want a deeper breakdown? Read this guide on how to save money from salary — it walks you through the exact sequence, step by step.

Why Saving Feels Impossible on a Low Income (Real Truth)

Most financial advice online is written for people earning ₹50,000+. When you earn ₹15,000, reading that advice feels like a joke. ‘Invest in mutual funds.’ ‘Cut your gym membership.’ You don’t have a gym membership.

Here’s the actual reason saving feels impossible on a tight salary:

There’s no buffer. When you earn just enough to cover basics, any small unexpected expense — a medical bill, a broken phone screen, a bus pass — destroys the entire month’s budget.

Social pressure is real. Your colleague orders biryani. You feel weird eating a packed lunch. This is one of the biggest hidden drains for low-income earners.

No system = chaos. Without a plan, money flows wherever it’s easiest to spend. UPI, EMIs, and apps are all designed to make you spend more.

The good news? All three of these are fixable. Not with willpower — with a simple system.

The 5-Step Fast Saving System (Works Even on ₹15,000 Income)

I call this the ‘Save Before You Spend’ system. It’s simple, it’s boring, and it works.

Step 1: Set a Fixed Saving Number (Not a Percentage)

Percentages feel abstract. A fixed number is real. Decide right now: ‘I will save ₹800 every month.’ That’s it. Don’t worry about 10% or 20%. Just pick a number you can do without failing.

Step 2: Open a Separate Savings Account

Not a different bank. Just a second account in the same bank. Transfer your saved amount there on salary day. Don’t get a debit card for this account. Make it inconvenient to access.

Step 3: Know Your 4 Expense Categories

Every rupee you spend falls into one of four buckets:

- Fixed needs: Rent, EMI, mobile, electricity

- Variable needs: Groceries, transport, medicines

- Wants: Food delivery, outings, shopping

- Savings: Your untouchable money

Most people have no idea how much they spend on ‘wants.’ Track it for just 7 days. You’ll be shocked.

Step 4: Set a Daily Spending Limit

Take your ‘variable needs + wants’ budget and divide by 30. That’s your daily limit. On ₹15,000 income, this might be ₹180–₹220 per day. Write it on your phone’s lock screen.

Step 5: Review Every Sunday Night (10 Minutes)

Look at what you spent. No guilt. Just facts. Ask: where did I overspend? What can I adjust next week? This weekly check-in builds the habit of awareness — which is 80% of saving.

For a complete walkthrough, check out this step-by-step monthly saving method that pairs perfectly with this system.

Clever Ways to Save Money That Actually Work

These aren’t generic tips. These are things I’ve personally recommended — and seen work — with real people on real low salaries.

- Cook 3 extra meals at home per week. Even switching from ₹80 restaurant meals to ₹25 home meals 3 times a week saves ₹660/month minimum.

- Buy vegetables at a local sabji mandi, not in a supermarket. You can save 30–40% on fresh produce easily.

- Use only one OTT platform at a time. Rotate between Netflix, Amazon Prime, and Hotstar across months instead of all at once.

- Switch to a ₹179 or ₹199 mobile prepaid plan. Many people pay ₹399+ when they don’t need more than 2GB/day.

- Use the 48-hour rule for online shopping. Add to cart. Wait 48 hours. Most impulse wants disappear.

- Take your lunch to work. One packed lunch daily = ₹1,200–₹1,800 saved every month.

- Set your UPI payment limit low. Keep daily UPI limit at ₹2,000 via your banking app. Makes you more deliberate.

How to Save Money with 20,000 Salary (Real Example)

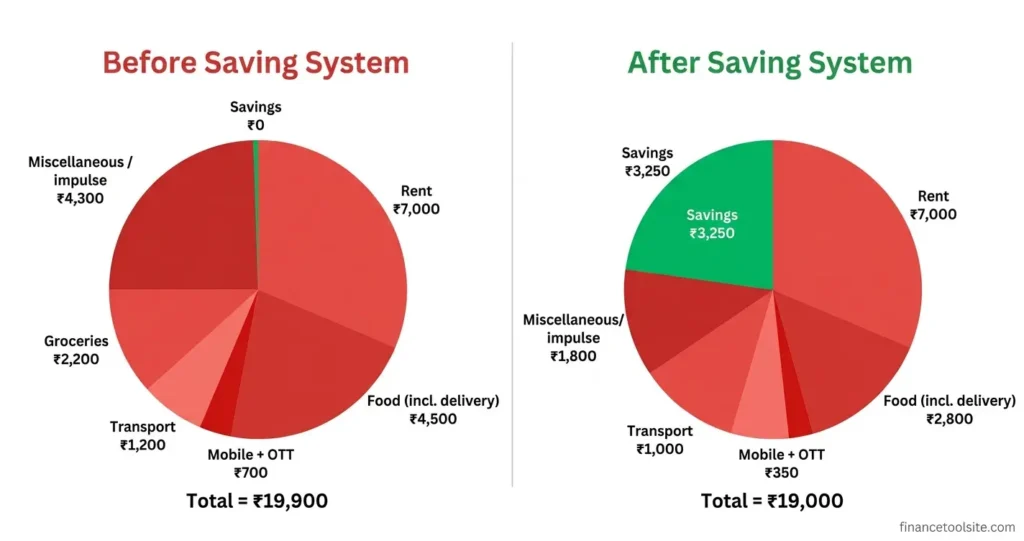

Let’s talk about Ramesh. 27 years old. Factory supervisor in Pune. Monthly salary: ₹20,000. He came to me saying he had zero savings after 4 years of working.

Here’s what his money was actually doing:

| Category | Before (₹) | After System (₹) |

| Rent | 7,000 | 7,000 |

| Food (incl. delivery) | 4,500 | 2,800 |

| Mobile + OTT | 700 | 350 |

| Transport | 1,200 | 1,000 |

| Groceries | 2,200 | 1,800 |

| Miscellaneous / impulse | 4,300 | 1,800 |

| Savings | 0 | 3,250 |

Ramesh saved ₹3,250 per month with zero sacrifice on basics — just discipline on food delivery and impulse purchases. In 12 months, that’s ₹39,000. Enough for an emergency fund and some left to start a small SIP.

Want to calculate your own saving potential? Try the free money management calculator — it gives you a clear picture in minutes.

Top 10 Brilliant Money Saving Tips (Practical)

Here are ten practical tips that have the highest real-world impact for low-income earners:

- Save the same day your salary arrives. Not at the end of the month.

- Delete food delivery apps for 15 days/month. This one habit saves ₹800–₹1,500 for most people.

- Write down every expense for one week. You will find at least one ₹500 leak.

- Buy in bulk. Rice, dal, cooking oil, soap — monthly bulk purchase always beats daily small purchases.

- Avoid ‘just ₹99’ subscriptions. They add up to ₹500–₹1,000 monthly unnoticed.

- Learn to say no. Social spending — chai rounds, birthday treats, group outings — is often your biggest invisible cost.

- Walk or cycle for short distances. Cuts auto and Uber spending by ₹300–₹700/month for many people.

- Set a grocery list before shopping — and stick to it. Unplanned grocery trips cost 25–30% more.

- Use your savings goal as motivation. Write it down: ‘I’m saving for a phone / emergency fund / my child’s school fee.’ A goal makes denial easier.

- Increase your saving by ₹100 every 3 months. Small increases build massive momentum over a year.

Set your first goal using this savings goal calculator — it tells you exactly how long it takes to reach your target.

Realistic Ways to Save Money Without Stress

Saving doesn’t have to feel like punishment. Most people quit because saving feels restrictive. Here’s how to make it sustainable:

- Start embarrassingly small. ₹200 per month is still infinitely better than ₹0. Build the habit first, the amount second.

- Allow one small treat per week. A ₹100 street food meal you enjoy deliberately is better than three ₹150 impulse orders you regret.

- Don’t aim for perfection. If you overspend one week, just restart. A bad week doesn’t mean a bad month.

- Celebrate every milestone. First ₹1,000 saved? Note it. First ₹5,000? Tell someone you trust. Small wins build identity.

- Make saving visible. Keep a chart on your wall or phone wallpaper. ‘I saved ₹800 this month’ — seeing it matters.

These are the realistic ways to save money that actually stick long-term — because they work with human behaviour, not against it.

Mistakes That Keep You Broke

I’ve seen the same mistakes ruin months of saving. Avoid these:

- Saving what’s ‘left over.’ There will never be anything left over unless you save first.

- Keeping savings in your regular account. If it’s accessible, you will spend it. Full stop.

- Borrowing from savings for ‘small’ things. ₹500 from savings here, ₹300 there — your fund disappears in a month.

- No tracking. ‘I’ll remember where the money went’ — you won’t. Write it down.

- Waiting for a raise to start saving. The habit must come first. The raise later. People who don’t save on ₹15,000 typically don’t save on ₹30,000 either.

Tools & Calculators That Make Saving Easy

You don’t need expensive apps. These free tools are enough:

- Money Management Calculator — See exactly where your money goes each month

- Savings Goal Calculator — Set a target and find out how long it takes to get there

- SIP Calculator — When you’re ready to invest your savings, see how a small monthly SIP grows

For reference on average Indian household saving rates, the Reserve Bank of India publishes annual household savings data that gives useful context on where most Indians stand financially.

FAQ — Your Questions Answered

How to save money fast on a low income in India?

Start by saving a fixed amount — even ₹500 — the same day your salary arrives. Put it in a separate account you don’t touch. Then cut the two biggest leaks: food delivery and impulse purchases. For most people earning ₹10,000–₹20,000, this alone saves ₹1,500–₹3,000 per month.

How to save money fast on a low income from salary?

The moment your salary is credited, immediately transfer your saving amount to a separate account. Pay fixed bills next. Only then look at what’s left to live on. This ‘save first’ system is the single biggest behaviour change that moves people from zero savings to consistent savings.

How to save money with 20,000 salary?

On a ₹20,000 salary, a realistic monthly saving goal is ₹2,000–₹3,500. Break your expenses into rent, groceries, transport, and daily spending. Cut food delivery to 2–3 times a week maximum. Cook at home more often. Track every purchase for 30 days — most people find at least ₹1,500 in leaks they didn’t realise existed.

What are clever ways to save money on a low income?

Buy groceries in bulk, carry a packed lunch to work, delete delivery apps when you’re bored, use the 48-hour rule before online purchases, share OTT subscriptions with family, and switch to a cheaper mobile plan. None of these require any special income — just awareness and small daily decisions.

What are realistic ways to save money without feeling deprived?

Start with a number you can save without any stress — even ₹200 a month. Build the habit. Allow yourself one small weekly treat that you plan for. Don’t aim for perfection; aim for consistency. Over 12 months, even ₹500/month becomes ₹6,000 — which is more than most people in this income bracket manage to save at all.

Is there a salary calculator to help save money?

Yes. Use the free money management calculator to plan your monthly budget by salary. It shows how to save money from salary with a clear category-wise split.

Final Words: Start Today, Not Next Month

Here’s something I tell almost everyone who says they can’t save on their salary: the system matters more than the amount. You don’t need ₹5,000 a month to make progress. You just need to start — even ₹200, ₹500 — but start now, not “next month.”

If you’ve been trying to figure out how to save money fast on a low income, understand this: it’s not about being a financial expert. It’s about doing a few simple things consistently — saving before you spend, cutting the biggest money leaks, and tracking where your money actually goes. That’s it. No complicated formulas. No unrealistic advice.

And once you start following this, you’ll realize something important — even on a low income, saving is possible. Not perfect, not huge in the beginning, but real and consistent. You already know what to do.

Now it’s just about taking action — starting with your very next salary.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. Individual financial situations may vary, so consider your personal circumstances before making any financial decisions.

1 thought on “How to Save Money Fast on a Low Income (Stop This One Mistake Today)”