The moment your salary hits your account is the most important financial moment of your entire month — but most people don’t treat it that way. They check their balance, feel a quick sense of relief, and then let the next 24–48 hours quietly wipe out any chance of saving. If you’ve been trying to figure out how to save money from salary and still end up with nothing left, the problem isn’t your income or lack of discipline. It’s what you do in those first few hours after getting paid.

I’ve seen this pattern play out for years. Whether someone earns ₹20,000 or ₹80,000, the mistake is the same: spend first, save later. And later never comes. By the end of the month, there’s barely anything left to save. This article is designed to change that — with a simple, practical action plan you can follow the very next time your salary is credited.

Table of Contents

What to Do After Salary Credit

How to save money from salary in 5 immediate steps:

- Transfer your savings amount to a separate account within 2 hours of salary credit.

- Pay all fixed obligations (rent, EMIs, SIPs) on the same day or the next morning.

- Set a fixed weekly spending limit in cash or UPI — not “whatever’s left.”

- Delete food delivery and shopping apps (or hide them) for the first 3 days.

- Log your salary-day actions in one note so the habit repeats automatically next month.

What to Do Right After Your Salary Hits Your Account

The first thing most people do after a salary credit? Open a food delivery app or start planning an outing. It feels harmless in the moment, but this is exactly where your savings quietly disappear.

The smarter move is actually quite boring — and that’s why it works. Within the first couple of hours of your salary being credited, you need to move your savings out of your main account. Not later. Not after spending. Immediately.

Think of your savings account like a locked space. The longer money sits in your primary account, the easier it is to spend it without thinking. But the moment you transfer it out, your mind adjusts to what’s left. This simple habit builds discipline over time, which is also why many people prefer structured options like government-backed small savings schemes in India to keep their money separate and harder to spend.

Decide your savings amount before your salary even arrives. Even ₹1,500 on a ₹15,000 salary is a strong start. Transfer it first — then manage everything else around what’s left.

Why Most People Still Fail to Save Money from Salary

Here’s the painful truth: most people fail to save money from salary not because they earn too little — but because they have no system for the first 24 hours.

I’ve counselled people earning ₹60,000 a month who had zero savings. And I’ve seen people on ₹22,000 who had a growing emergency fund and an active SIP. The difference? A deliberate salary-day habit versus no habit at all.

The three patterns I see constantly:

- “Treat yourself” spending right after payday. That one dinner, that one Amazon order — it sets the psychological tone for the entire month.

- Paying bills whenever they come in instead of clearing everything on one designated day. This creates constant uncertainty about your real balance.

- No savings target set in advance. “I’ll save whatever’s left” is not a plan. It’s wishful thinking.

The fix is a system — one you set up once and follow mechanically. Let’s build it.

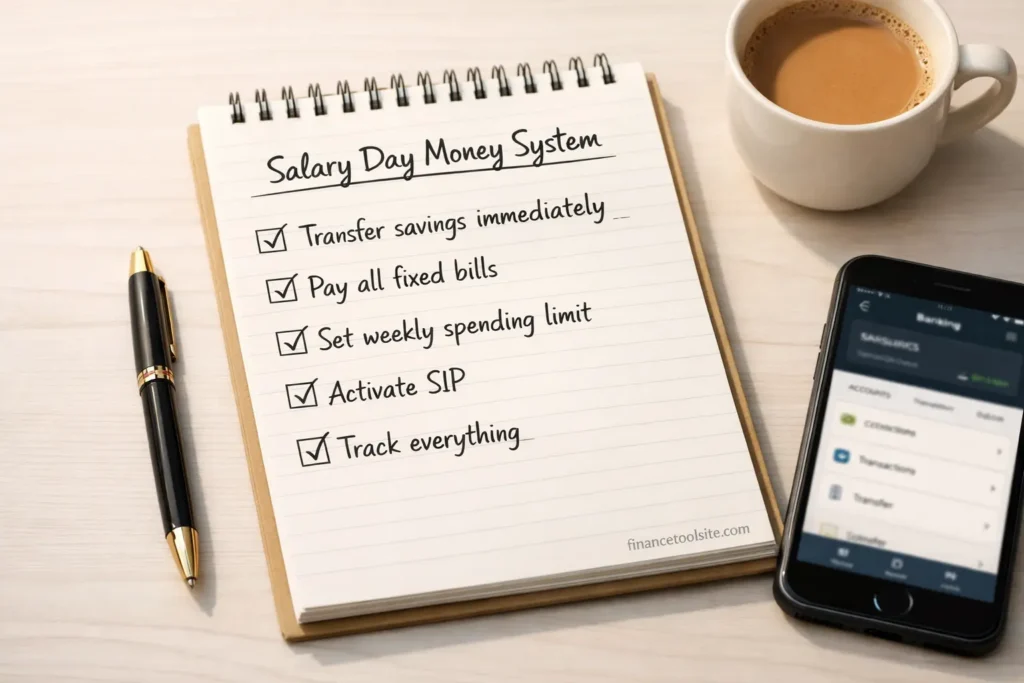

The 5-Step Salary Day System

This is the system I’ve helped hundreds of clients implement. It takes about 20 minutes on salary day and makes the entire rest of the month easier.

- Transfer savings immediately: Decide your savings amount in advance (even 10% of salary). The moment your salary is credited, open your banking app and move that amount to a separate savings account. Don’t think. Just do it.

- Pay all fixed bills on the same day: Rent, EMIs, credit card dues, insurance premiums — pay all of these on salary day itself. What remains is your actual spendable balance. No guessing games.

- Set a weekly cash limit: Divide your remaining balance by 4 (weeks). That weekly number is your maximum spend. Write it down. Stick to it. This prevents mid-month panic.

- Activate your SIP on salary day: If you have a mutual fund SIP, set the auto-debit date to 1 or 2 days after your salary credit. Investing becomes automatic. (Check a SIP calculator to see what even ₹500/month becomes in 10 years.)

- Log it all in one note: Take 5 minutes to write: salary received, savings transferred, bills paid, weekly budget. This 5-minute note makes next month’s salary day twice as fast.

Set This Up in Your Bank (Automation Trick)

The best saving decision you’ll ever make is removing yourself from the equation entirely.

Most Indian banks — including SBI, HDFC, ICICI, and Kotak — allow you to set up a standing instruction (SI) or auto-transfer. You can schedule a fixed amount to move from your salary account to your savings or RD account on a set date every month.

Set it for 1–2 days after your salary credit date. You won’t even see the money. It’s gone before your brain registers it as available.

Pro tip: Open a zero-balance savings account with a different bank for your “savings only” account. The slight friction of logging into a different app before spending your savings is often enough to stop impulse withdrawals.

If you want to go further, link your SIP auto-debit to the same date. Many disciplined savers also combine this with options like the National Pension System (NPS) for long-term savings, which encourages consistent investing through automated contributions. Within one setup session, your entire fixed obligation structure runs on its own.

For a full month-by-month structure after this initial setup, follow this step-by-step monthly saving method — it picks up exactly where salary day leaves off.

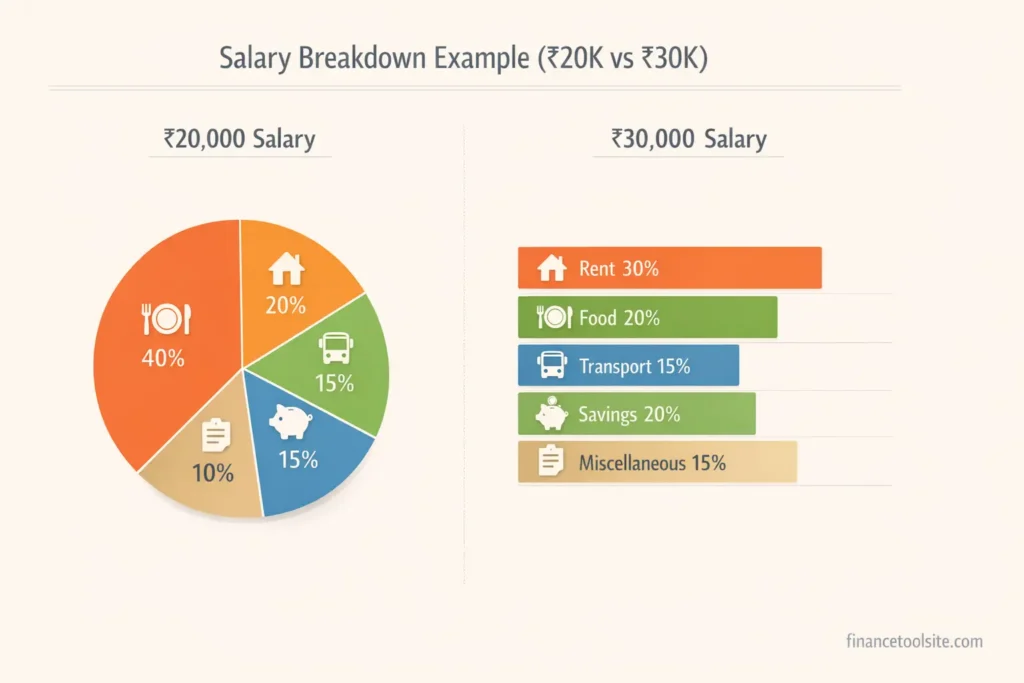

Real Example: ₹20,000 vs ₹30,000 Salary Breakdown

Let me show you what salary day looks like in practice. These are real-world numbers, not textbook scenarios.

Salary: ₹20,000/month

| Category | Amount | When to Pay |

|---|---|---|

| 💰 Savings (transfer first) | ₹2,000 (10%) | Within 2 hours of credit |

| 🏠 Rent | ₹5,500 | Salary day |

| 📦 Groceries & household | ₹3,000 | Weekly limit: ₹750 |

| 🚌 Transport | ₹1,500 | Weekly limit: ₹375 |

| 📱 Mobile + internet | ₹500 | Salary day |

| 🍱 Food (eating out/delivery) | ₹2,500 | Weekly limit: ₹625 |

| 🛒 Personal/misc | ₹2,000 | Weekly limit: ₹500 |

| 🆘 Emergency buffer | ₹3,000 | Do NOT touch |

| Total | ₹20,000 |

Salary: ₹30,000/month

| Category | Amount | When to Pay |

|---|---|---|

| 💰 Savings (transfer first) | ₹4,500 (15%) | Within 2 hours of credit |

| 🏠 Rent | ₹7,000 | Salary day |

| 📦 Groceries & household | ₹4,000 | Weekly limit: ₹1,000 |

| 🚌 Transport | ₹2,000 | Weekly limit: ₹500 |

| 📱 Mobile + internet | ₹700 | Salary day |

| 🍱 Food (eating out/delivery) | ₹3,500 | Weekly limit: ₹875 |

| 💳 EMI / SIP | ₹3,000 | Auto-debit day 1–2 |

| 🛒 Personal/misc | ₹2,300 | Weekly limit: ₹575 |

| 🆘 Emergency buffer | ₹3,000 | Do NOT touch |

| Total | ₹30,000 |

Use a money management calculator to build your own version of this breakdown based on your exact salary and expenses.

Mistakes That Kill Your Savings on Day 1

I’ve watched people build a solid salary-day system and then blow it on the very same day. Here are the biggest culprits:

- Ordering food to “celebrate” salary day. One Swiggy order triggers the “I’ve been good, I deserve this” mindset — and it snowballs fast.

- Checking bank balance and feeling rich. Before you’ve transferred savings or paid bills, that number is not yours to spend. Never make financial decisions at this moment.

- Buying things you “needed” all month. All the things you held off on buying while broke — clothes, gadgets, accessories — suddenly feel urgent. They’re not. Wait 72 hours.

- Lending to friends and family immediately. “Bhai abhi toh salary aaya hai” is the most expensive sentence in personal finance. Set a policy: no lending in the first week.

- Skipping the savings transfer “just this month.” There will always be a reason. Once you skip, you’ll skip again. Non-negotiable: transfer savings first, always.

“The first 24 hours after salary credit decide the entire month. Get those hours right, and saving becomes effortless.”

Smart Ways to Control Spending — Practical Indian Tips

Knowing your budget and actually living within it are two different things. Here’s what works in practice:

Use UPI limits to control impulse spending. Most UPI apps let you set daily transaction limits. Set yours to your daily budget — not your full salary. The friction of “UPI limit exceeded” stops thoughtless taps.

Switch to weekly grocery shopping. Monthly bulk shopping leads to waste. Weekly trips with a list keep food costs predictable and prevent the “might as well grab this too” behaviour.

Delete (or bury) Zomato, Swiggy, and Blinkit for the first 3 days of the month. That’s the highest-risk window. One habit of cooking at home for 3 days locks in a momentum you’ll likely carry forward.

The “sleep on it” rule for anything above ₹500. If you see something you want to buy online, add it to a wishlist and revisit in 48 hours. 80% of the time, the urge passes.

Keep one “guilt-free” amount every week. Give yourself ₹200–₹500 to spend on absolutely anything with zero tracking. This prevents the psychological deprivation that causes binge spending later.

According to RBI household finance research, the primary reason Indian salaried households don’t save consistently is the absence of a structured spending system — not the lack of income. Your income isn’t the problem. Your system is.

Tools That Make Saving Effortless

You don’t need complicated apps. You need the right 3–4 tools used consistently.

Build your personal salary breakdown in minutes.

See exactly how long to reach any savings target.

What ₹500/month becomes in 10 years will surprise you.

The full month-by-month system after salary day is set up.

Beyond calculators, use your bank’s standing instruction feature + one simple note (Google Keep or even a paper notebook) to log salary-day actions. That’s genuinely all you need.

FAQ — How to Save Money from Salary

Q: How to save money from salary in India?

To learn how to save money from salary in India, start by transferring 10–20% of your income to a separate savings account as soon as your salary is credited. Then manage the rest for rent, food, and daily expenses. Automating this process makes saving consistent and removes the need for willpower.

Q: How to save money with ₹20,000 salary?

With a ₹20,000 salary, you can save ₹2,000–₹4,000 by controlling rent, reducing food delivery, and cutting small daily expenses. The key is to save first on salary day and adjust your spending with the remaining amount.

Q: How to save money with ₹10,000 salary?

If your salary is ₹10,000, start small by saving ₹500–₹1,000 every month. Focus on essential expenses, avoid unnecessary spending, and gradually increase your savings as your income grows. Consistency matters more than the amount.

Q: How to save money from salary in bank automatically?

To save money from salary automatically in a bank, set up an auto-transfer or standing instruction that moves a fixed amount to a separate savings account right after your salary is credited. This ensures saving happens before spending.

Q: What are clever ways to save money from salary?

Some clever ways to save money from salary include automating savings, setting a weekly spending limit, using the 24-hour rule before purchases, and avoiding impulse spending on salary day. Small behavior changes can lead to big savings over time.

Q: How to save money from salary ₹15,000?

With a ₹15,000 salary, aim to save at least ₹1,500–₹3,000 by prioritizing essential expenses and cutting non-essential spending like subscriptions and frequent eating out. Even small, consistent savings build strong financial habits.

Q: Is there a calculator to plan how to save money from salary?

Yes, using a salary saving or money management calculator helps you understand how much you can save based on your income and expenses. It gives a clear breakdown and makes financial planning easier.

Summary

Saving money from your salary is not about how much you earn, but what you do right after you get paid. By transferring a fixed amount to savings first, controlling early spending, and following a simple system, you can build consistent savings every month. Even small amounts, saved regularly, can grow into a strong financial habit over time.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Please consult a qualified financial advisor before making any financial or investment decisions.

1 thought on “How to Save Money from Salary – Do This Within 24 Hours of Getting Paid”