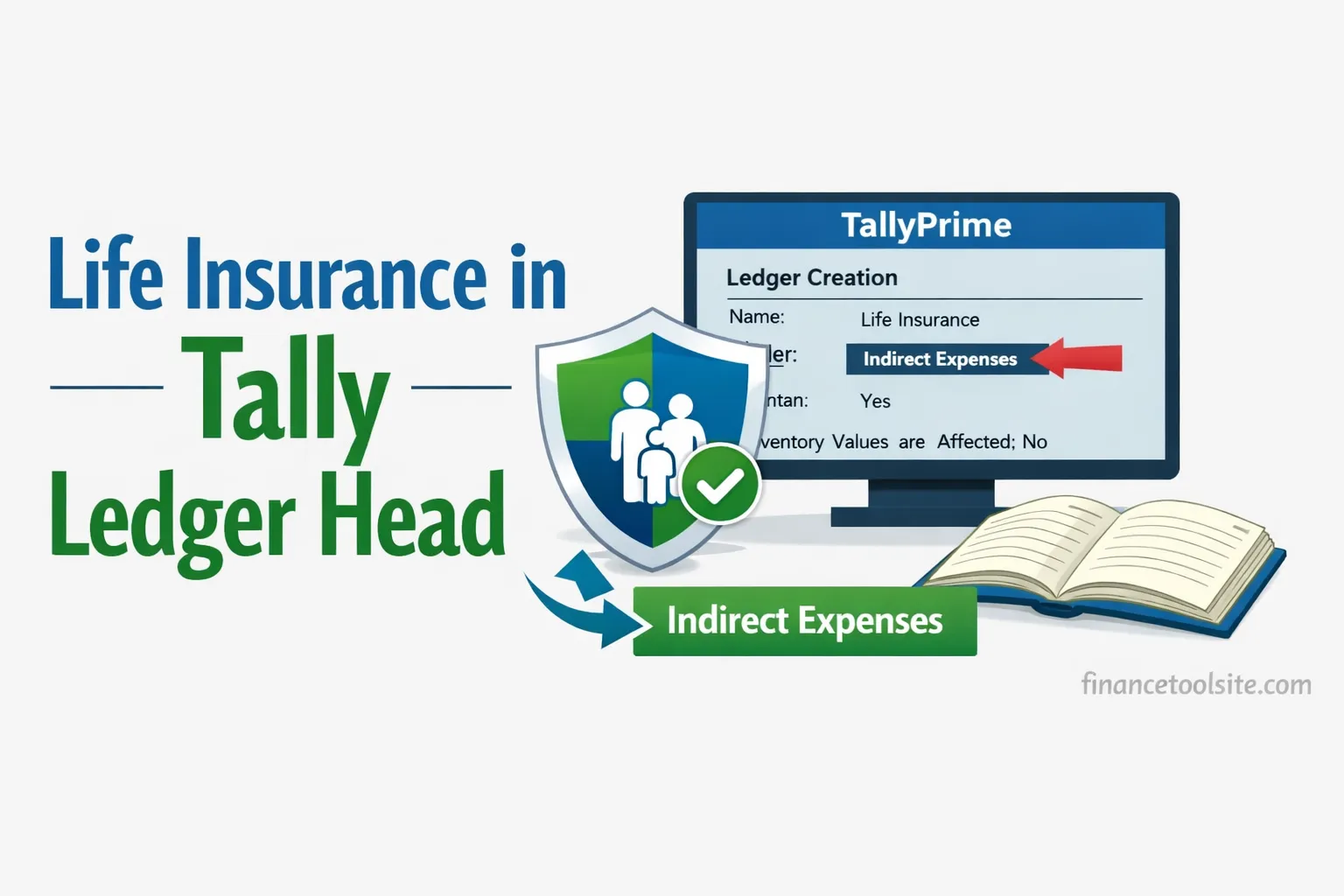

If you are wondering life insurance under which head in Tally, you are not alone. Many beginners and small business accountants get confused while choosing the correct ledger group for insurance payments. In most business situations, life insurance premiums are recorded under Indirect Expenses in Tally, whether you are using Tally ERP 9 or Tally Prime.

This classification follows normal accounting principles where expenses that support business operations but are not directly linked to production are treated as indirect expenses. Insurance-related rules and financial regulations in India are also governed by the Insurance Regulatory and Development Authority of India (IRDAI), which explains how insurance works in the financial system.

However, there is one important exception that accountants always remember. If the business bank account is used to pay the owner’s personal life insurance policy, the payment should not be treated as a business expense. In that case, the correct ledger head is Drawings, because the business is paying a personal expense of the owner.

Quick Answer:

If you are searching life insurance under which head in Tally, the correct ledger group in most cases is Indirect Expenses. If the premium is for the owner’s personal policy paid from the business account, record it under Drawings. Employee group life insurance paid by the company is usually recorded under Staff Welfare Expenses.

If you want to estimate the cost of a policy quickly, you can also use this:

Table of Contents

3 Simple Ledger Rules for Life Insurance in Tally

When deciding life insurance under which head in Tally, accountants usually follow three simple rules based on the purpose of the insurance payment.

Rule 1: Business Life Insurance → Indirect Expenses

If the life insurance premium is paid for business purposes, such as a keyman insurance policy or business protection plan, it should be recorded under Indirect Expenses in Tally.

Rule 2: Employee Group Insurance → Staff Welfare Expenses

If the company pays group life insurance for employees, the expense is usually recorded under Staff Welfare Expenses, since it is part of employee benefits.

Rule 3: Owner’s Personal Insurance → Drawings

If the business account is used to pay the owner’s personal life insurance premium, it should not be treated as a business expense. Instead, it must be recorded under Drawings.

Once you understand these three simple rules, deciding life insurance under which head in Tally becomes much easier while creating ledgers or recording payments.

Life Insurance Under Which Head in Tally

When accountants discuss life insurance under which head in Tally, the correct ledger group in most cases is Indirect Expenses. Any life insurance premium paid for business purposes—such as a keyman insurance policy or group life insurance for employees—is treated as a normal operating expense of the business.

In Tally Prime, this simply means that while creating the ledger for the insurance premium, the ledger group should be selected as Indirect Expenses. This classification follows standard accounting principles used in financial reporting. Even the International Financial Reporting Standards (IFRS) explain that operating costs that support business activities but are not directly linked to production are treated as operating or indirect expenses.

This is where many beginners get confused. Because insurance is an important cost for the business, some people assume it should be recorded under Direct Expenses. In practice, that classification is incorrect. Direct expenses are costs directly related to producing goods or delivering services—such as raw materials, manufacturing labour, or freight inward.

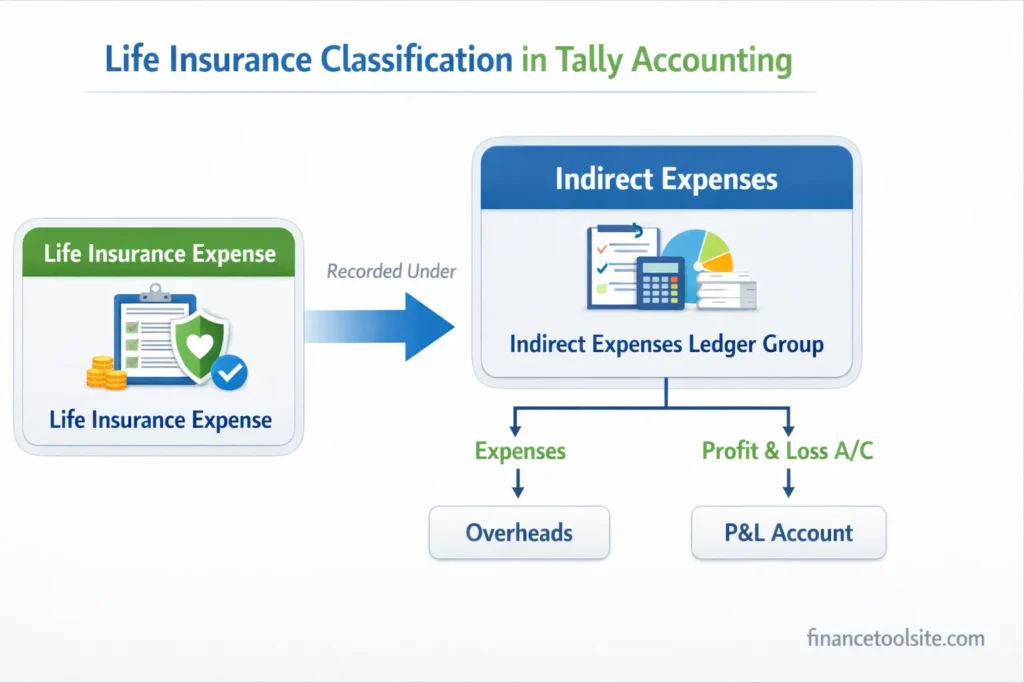

Life insurance works differently. It does not help produce goods or services. Instead, it protects the business or the people working in it. That is why accountants treat life insurance as an operating expense, which falls under Indirect Expenses in Tally.

If you want to understand how other types of insurance are recorded in Tally, you can also read this detailed guide on insurance under which head in Tally.

Once you understand this simple accounting logic, selecting the correct ledger group while recording insurance payments in Tally becomes much easier.

Why Life Insurance Comes Under Indirect Expenses

Before creating the ledger, it is useful to understand the accounting logic behind life insurance under which head in Tally. Once this concept is clear, selecting the correct ledger group while recording insurance payments in Tally Prime becomes much easier.

In basic accounting, business expenses are generally divided into two main categories:

Direct Expenses – These are costs that are directly connected to producing goods or delivering a service. Common examples include raw materials, manufacturing labour, freight inward, and other production-related costs.

Indirect Expenses – These are expenses that help operate the business but are not directly involved in producing a product or service. Typical examples include salaries, office rent, electricity bills, administrative costs, and insurance premiums.

Life insurance clearly falls into the second category. When a company pays a life insurance premium—for example a keyman insurance policy or a group life insurance plan for employees—the purpose is financial protection for the business rather than production support.

Because of this, accountants normally record life insurance premiums as Indirect Expenses in Tally. This ensures that the cost appears correctly in the Profit & Loss account as part of operating expenses.

Another point supporting this classification comes from taxation rules. Under the Income Tax Department of India, certain insurance premiums paid for legitimate business purposes can be treated as business expenses. This is one reason accountants commonly classify them under Indirect Expenses in Tally.

If you want to understand how other similar expenses are grouped in Tally, you can also read this guide on commission under which group in Tally.

Once you understand this accounting logic, the answer to life insurance under which head in Tally becomes straightforward—in most cases, it is recorded under Indirect Expenses.

Ledger Head Table for Different Situations

In practice, the correct ledger head depends on who the insurance policy is meant for. Not every insurance payment is recorded in the same ledger group. The table below shows the most common situations accountants deal with while recording insurance in Tally.

| Situation | Ledger Head in Tally |

|---|---|

| Business Keyman Life Insurance | Indirect Expenses |

| Group Life Insurance for Employees | Staff Welfare Expenses |

| Owner’s Personal Life Insurance (paid from business account) | Drawings |

| Director’s Life Insurance (for business purpose) | Indirect Expenses |

| Vehicle Insurance for Business Vehicle | Indirect Expenses |

| Fire / Property Insurance | Indirect Expenses |

This covers most real-world scenarios you will see while maintaining books in Tally. If you want to explore all available ledger groups in detail, you can also check the complete tally ledger group list on this website.

One important thing to remember: when the owner’s personal life insurance premium is paid from the business bank account, it should not be recorded as a business expense. Instead, it must be treated as Drawings, because the payment relates to the owner’s personal finances and not to the business itself.

This is a mistake many beginners make while learning Tally. Recording personal expenses under business expenses can distort the Profit & Loss statement and create issues later during balance sheet preparation or finalisation.

How to Record Life Insurance in Tally Prime (Step-by-Step)

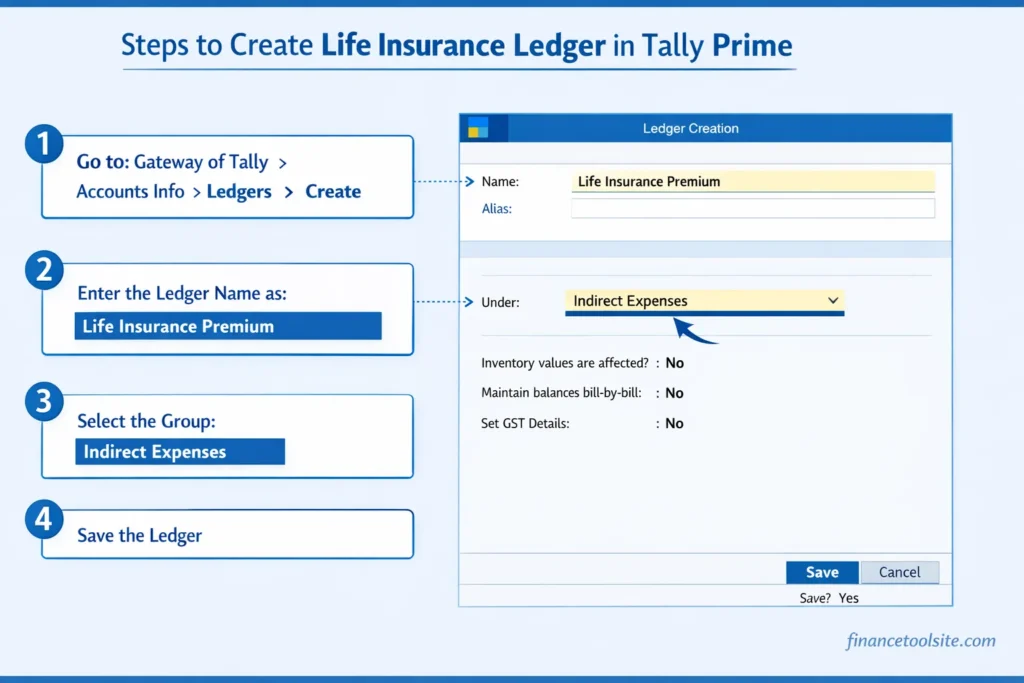

Once you understand that life insurance under which head in Tally is recorded under Indirect Expenses, the next step is creating the correct ledger in Tally Prime. The process is simple and only takes a minute.

Follow these steps to create the ledger:

- Open Tally Prime and load your company data.

- Press G (Go To) or open the Chart of Accounts from the main menu.

- Select Ledger to view the list of existing ledgers.

- Press Alt + C to create a new ledger.

- In the Name field, enter a suitable name such as Life Insurance Premium or the specific policy name.

- In the Under (Group) field, choose Indirect Expenses.

- Leave the Opening Balance as zero unless there is a balance carried forward from the previous year.

- Press Ctrl + A to save the ledger.

After saving, the Life Insurance Premium ledger will be available whenever you record insurance payments.

If you are entering the premium payment immediately, open the Payment Voucher (F5) in Tally Prime. Select the bank or cash account from which the payment is made, and debit the Life Insurance Premium ledger you just created.

Once the entry is saved, the insurance premium will automatically appear under Indirect Expenses in the Profit & Loss account.

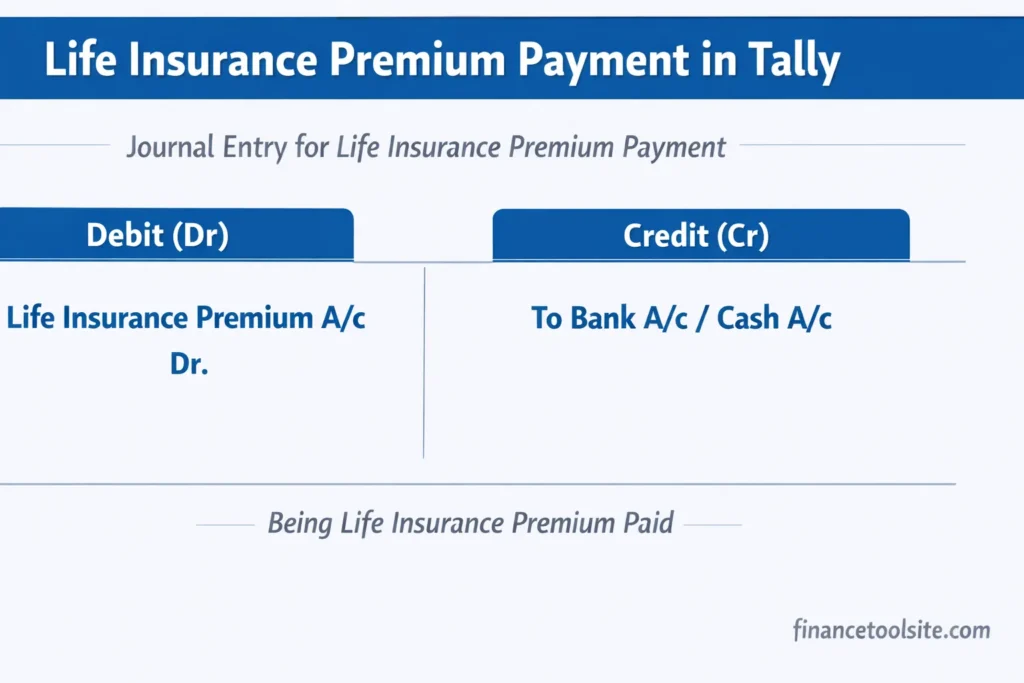

Journal Entry for Life Insurance in Tally

Once the ledger is created, the next step is recording the life insurance premium payment. In accounting terms, the premium is treated as an expense, so the Life Insurance Premium account is debited, while the bank or cash account is credited.

The basic journal entry looks like this:

| Account | Debit | Credit |

|---|---|---|

| Life Insurance Premium A/c | ₹ Amount | — |

| To Bank A/c / Cash A/c | — | ₹ Amount |

Narration: Being life insurance premium paid for policyname/period.

In Tally Prime, this transaction is usually recorded using a Payment Voucher (F5) instead of a Journal Voucher. The reason is simple: whenever money goes out of the bank or cash account, Tally expects the entry to be recorded through the payment voucher.

So in practice, you only need to select the Life Insurance Premium ledger as the debit account, and Tally will automatically credit the bank or cash account used for the payment.

One more situation worth understanding is prepaid insurance. Sometimes businesses pay insurance premiums in advance for a full year. In such cases, instead of recording the entire amount as an expense immediately, accountants may first debit Prepaid Insurance (under Current Assets). Then, every month a portion of that amount is transferred to the Life Insurance Premium expense account.

This approach is commonly used by businesses that prepare monthly financial statements, because it spreads the insurance cost across the correct accounting period.

Practical Example of Life Insurance Entry

To understand this more clearly, let’s look at a simple real-world example.

Suppose Rajesh Enterprises pays ₹18,000 per year as a Keyman Life Insurance premium for its proprietor. The payment is made directly from the company’s HDFC Bank account.

In this case, the insurance is meant to protect the business, so it is treated as a normal operating expense. Since we already know that life insurance under which head in Tally is usually recorded under Indirect Expenses, the entry would look like this:

| Account | Debit | Credit |

|---|---|---|

| Life Insurance Premium A/c | ₹18,000 | — |

| To HDFC Bank A/c | — | ₹18,000 |

Narration: Keyman life insurance premium paid via HDFC Bank for FY 2024–25.

The Life Insurance Premium ledger will be grouped under Indirect Expenses. Once recorded, this expense will appear in the Profit & Loss account of the business when you view the P&L report in Tally.

Example 2: Personal Life Insurance Paid from Business Account

Now consider a slightly different situation.

Assume the same owner pays his personal LIC policy premium of ₹12,000 from the company’s bank account. Even though the payment is made using the business bank account, the policy belongs to the owner personally, not to the business.

In such cases, the entry should not be recorded as a business expense. Instead, it must be treated as Drawings, because the business is paying a personal expense on behalf of the owner.

The correct entry would be:

| Account | Debit | Credit |

|---|---|---|

| Drawings A/c (Owner’s Name) | ₹12,000 | — |

| To HDFC Bank A/c | — | ₹12,000 |

Narration: Personal LIC premium of proprietor paid from business bank account, treated as drawings.

Recording it this way keeps the business expenses accurate and prevents personal costs from inflating the Indirect Expenses in the Profit & Loss account.

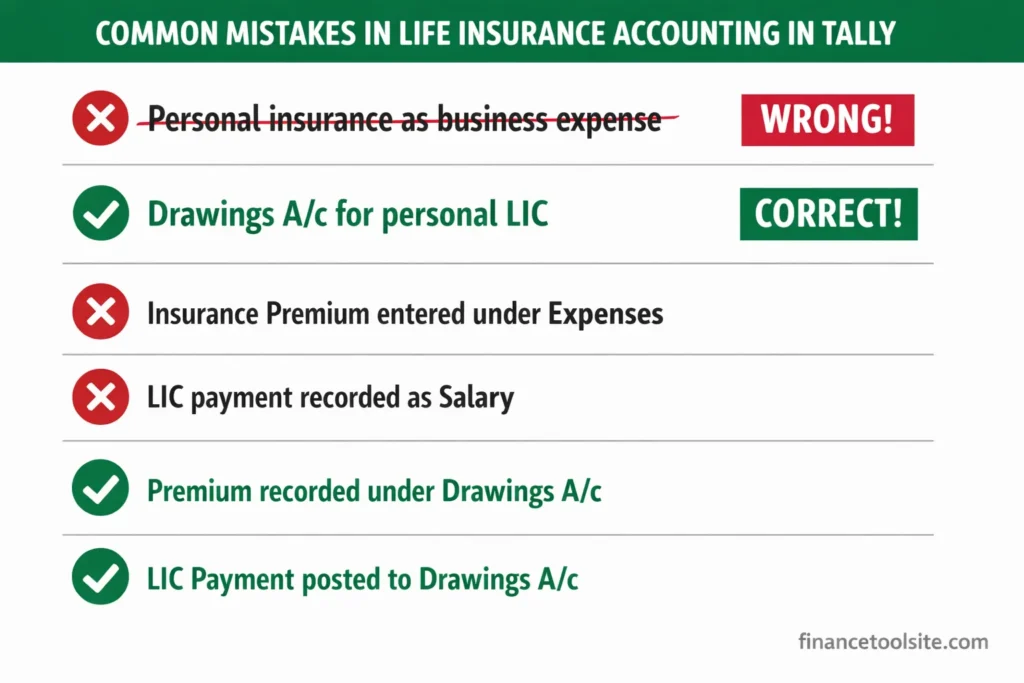

Common Mistakes Beginners Make

Even after understanding life insurance under which head in Tally, beginners still make a few common accounting mistakes. These errors usually happen because people mix personal expenses with business expenses or select the wrong ledger group.

Here are the most frequent issues I see while reviewing small business accounts:

Recording Personal Life Insurance as a Business Expense

This is probably the most common mistake beginners make when trying to understand life insurance under which head in Tally. When a business owner pays their personal LIC premium using the company’s bank account, many people incorrectly record the payment under Indirect Expenses.

However, that accounting treatment is not correct.

Since the policy belongs to the owner personally and not to the business, the payment should be recorded under Drawings, not as a business expense. If it is mistakenly recorded as an indirect expense, the Profit & Loss account will show higher expenses than the business actually incurred, which can distort financial statements.

In accounting principles, personal expenses of the owner must always be separated from business expenses. Financial reporting standards such as the Institute of Chartered Accountants of India (ICAI) also emphasize maintaining a clear distinction between business transactions and personal drawings.

If you are unsure about selecting the correct ledger group for different transactions, you can also check this complete Tally ledger group list.

Understanding this simple rule helps ensure that insurance entries are recorded correctly and prevents mistakes when deciding life insurance under which head in Tally.

Using the Wrong Ledger Group

Another mistake is placing the insurance ledger under groups like Current Liabilities or Provisions.

Once the premium is paid, it is no longer a liability. It becomes an expense of the business, which means it should normally be grouped under Indirect Expenses in Tally.

Choosing the wrong group can distort financial reports and make account analysis confusing later.

Not Separating Employee Insurance and Business Insurance

Businesses sometimes pay multiple types of insurance:

- Keyman insurance for business protection

- Group life insurance for employees

If both are recorded in the same ledger, it becomes difficult to understand how much the company spends on employee welfare versus business risk protection.

A better approach is:

- Keyman insurance → Indirect Expenses

- Employee group insurance → Staff Welfare Expenses

This keeps reporting clear and organised.

Recording Insurance as an Asset Instead of an Expense

Some beginners assume life insurance should be treated as an asset because policies sometimes have a surrender value.

However, when you are recording the regular premium payment, it is always treated as an expense.

Only in specific financial planning situations might accountants track the surrender value separately, but that is a different accounting treatment and not part of normal premium entries.

Using the Wrong Voucher Type

Another technical mistake is using a Journal Voucher when the premium is paid through the bank.

In Tally Prime, whenever money goes out of the bank or cash account, the correct voucher type is Payment Voucher (F5).

Journal vouchers are generally used for non-cash adjustments, so using them for bank payments can create confusion during voucher verification.

Many businesses also monitor their banking expenses separately to control costs. You can calculate your total monthly bank charges using this simple online tool:

Frequently Asked Questions

Q: Life insurance under which head in Tally?

A: In Tally, life insurance is usually recorded under Indirect Expenses. It is treated as an operating expense because it supports the business but is not directly related to production.

Q: Is life insurance a direct or indirect expense in Tally?

A: Life insurance is an Indirect Expense in Tally. It protects the business or employees but is not part of manufacturing or service delivery.

Q: Under which ledger group does insurance come in Tally?

A: Most insurance payments in Tally are recorded under Indirect Expenses. Employee insurance goes under Staff Welfare Expenses, and the owner’s personal insurance is recorded under Drawings.

Q: Can I claim personal life insurance as a business expense in Tally?

A: No. Personal life insurance of the owner should be recorded under Drawings, not as a business expense.

Q: What is the journal entry for life insurance premium in Tally?

A: The entry is: Life Insurance Premium A/c Dr → To Bank A/c / Cash A/c. In Tally Prime, this is usually recorded using Payment Voucher (F5).

Q: Where should group life insurance for employees be recorded in Tally?

A: Group life insurance for employees should be recorded under Staff Welfare Expenses in Tally.

Q: Is insurance included in indirect expenses in Tally?

A: Yes. Most business insurance like life insurance, vehicle insurance, and fire insurance is recorded under Indirect Expenses in Tally.

Q: How do I create a life insurance ledger in Tally Prime?

A: Go to Chart of Accounts → Ledger → Create, enter Life Insurance Premium, select Indirect Expenses, and save the ledger.

Q: What if the life insurance premium is paid in advance?

A: If paid in advance, record it under Prepaid Insurance (Current Assets) and transfer it to Life Insurance Premium as the expense period is used.

Summary

If you were searching life insurance under which head in Tally, the correct ledger group is Indirect Expenses for most business-related life insurance policies.

Employee group life insurance is recorded under Staff Welfare Expenses, while the owner’s personal life insurance paid from the business account should be treated as Drawings.

In Tally Prime, create the Life Insurance Premium ledger under the correct group and record the payment using Payment Voucher (F5) when cash or bank is involved.

Disclaimer: This article is for educational purposes only and does not constitute professional accounting advice. Always consult a qualified Chartered Accountant for advice specific to your business situation.

1 thought on “Life Insurance Under Which Head in Tally? 3 Simple Ledger Rules”